1 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

1700 G Street NW, Washington, DC 20552

Debt Collection Rule: Disclosing the Model

Validation Notice Itemization Table

October 29, 2021

This is a Compliance Aid issued by the Consumer Financial Protection Bureau. The Bureau published a Policy

Statement on Compliance Aids, available at

https://www.consumerfinance.gov/policy-compliance/rulemaking/final-

rules/policy-statement-compliance-aids/, that explains the Bureau’s approach to Compliance Aids.

1

An editable version of the model validation notice is available here.

1

The Debt Collection Rule (Rule) requires debt collectors to provide consumers with certain

information to help them identify the debt being collected. This information is called the

“validation information” and consists of information about the debt, information about the

consumer’s protections and rights during collection of the debt, and information to facilitate the

consumer’s ability to exercise those rights. The Rule details how a debt collector can provide the

validation information in a validation notice.

Appendix B of the Rule sets forth a model validation notice that a debt collector has the option to

use to provide the validation information. A debt collector is not required to use the model

validation notice. However, a debt collector who uses the model validation notice obtains a safe

harbor for the content and format requirements related to the validation information.

1

12 CFR

1006.34(d)(2); see also 12 CFR 1006.34(c) and 34(d)(1).

A debt collector also has the option to use a version of the model validation notice that adds or

omits certain optional content, a version that includes certain content on a separate page, or a

version that is otherwise substantially similar to the model validation notice. A debt collector who

2 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

uses one of these options also obtains a safe harbor for the content and format requirements

related to the validation information, except with respect to any content that appears on a separate

page. 12 CFR 1006.34(d)(2); see also 12 CFR 1006.34(c) and 34(d)(1).

However, because use of the model validation notice is not required, a debt collector also has the

option to provide the validation information using a form that is not substantially similar to the

model validation notice. Such a validation notice must still provide all of the required validation

information, and a debt collector who uses such a notice does not receive a safe harbor for the

content and format requirements of the Rule for the validation information provided. 12

CFR 1006.34(d)(2); see also 12 CFR 1006.34(c) and 34(d)(1).

2

This guidance document addresses how to provide certain validation information. This document

assumes use of the model validation notice.

3

Specifically, the Rule requires debt collectors to

include on the validation notice both the current amount of the debt and certain information about

the debt as of a particular date called the “itemization date.” Most of this required information

appears on the model validation notice in a tabular format.

Because this document assumes use of the model validation notice, it also assumes this

information will be disclosed in the tabular format. This document refers to that table as the

“Itemization Table” when providing guidance on the included disclosures. However, the concepts

discussed also apply more generally even if the model validation notice is not used.

2

More information about the validation information content and format requirements can be found in Section 12 of the

Debt Collection Rule Small Entity Compliance Guide

. Additionally, more information about the option to use the

model validation notice and how changes to the model validation notice affect the safe harbor for the validation

information content and format requirements can be found in the

Debt Collection Rule FAQs, Validation Information

Questions 2 through 4, as well as Section 12.1.3 of the Debt Collection Rule Small Entity Compliance Guide.

3

That is, this guidance document assumes a debt collector will use the model validation notice as it appears in

Appendix B of the Rule. This generally assumes that, among other things, a debt collector will not disclose certain

Itemization Table information on a separate page or use, for residential mortgage debt, the ability to substitute the

most recent periodic statement for some Itemization Table information (i.e., follow the special rule for residential

mortgage debt, or “Special Rule”). 12 CFR 1006.34(d)(2)(ii). As noted, a debt collector who uses either such option

retains the safe harbor for content and format requirements when using the model validation notice, except with

respect to content appearing on the separate page. However, some of the guidance discussed below may not apply, or

may apply differently, in such cases. For more information on the ability to disclose certain Itemization Table

information on a separate page, see footnote 8, below. For more information on the special rule for residential

mortgage debt, see footnotes 4 and 7, below and the

Debt Collection Rule FAQs, Validation Information: Residential

Mortgage Debt Questions.

3 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

This guidance document first provides an overview of the validation information contained in the

Itemization Table. It then illustrates steps a debt collector may take to complete the Itemization

Table. It also provides examples showing how a debt collector might complete the Itemization

Table for different types of debts.

Overview of the Itemization Table

Among other things, the validation notice generally

4

must include the following information about

the debt:

1. An itemization date. This is a reference date that occurs on or before the date the

validation notice is sent and on which the debt collector can ascertain the amount of the

debt. The itemization date is designed to reflect an event in the debt’s history that

consumers may recognize. The itemization date must be one of the following reference

dates: 1) the date of the last statement (generally from a creditor); 2) the charge-off date; 3)

the last payment date; 4) the transaction date; or 5) the judgment date. 12 CFR

1006.34(b)(3); 1006.34(c)(2)(vi).

2. The amount of the debt as of that itemization date. 12 CFR 1006.34(c)(2)(vii).

3. An itemization of the current amount of the debt that discloses categories of information

since the itemization date: 1) interest, 2) fees, 3) payments, and 4) credits. This guidance

document refers to these categories as the “Itemized Amounts.” Fields for the Itemized

Amounts must be included in the itemization, and the amounts cannot be left blank, even if

no additional amounts have been assessed or applied during the relevant time period. If

no additional amounts have been assessed or applied, a debt collector may include a zero

or “none,” or may state that no interest, fees, payments, or credits have been assessed or

applied to the debt. 12 CFR 1006.34(c)(2)(viii).

4. The current amount of the debt as of the date that the validation information is provided.

12 CFR 1006.34(c)(2)(ix).

4

Note that, if a debt collector uses the special rule for certain residential mortgage debt, discussed in footnote 3 above,

certain information, including the itemization date, is not required to be disclosed on the validation notice. However,

a debt collector must still determine the itemization date to disclose the other itemization-date dependent validation

information. See Debt Collection Rule FAQs, Validation Information: Residential Mortgage Debt Questions 2 and 5

.

4 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

These validation information requirements are discussed in more detail in the Debt Collection

Rule Small Entity Compliance Guide.

Generally, this validation information is required. A debt collector violates the Rule if any

required validation information is not disclosed to the consumer.

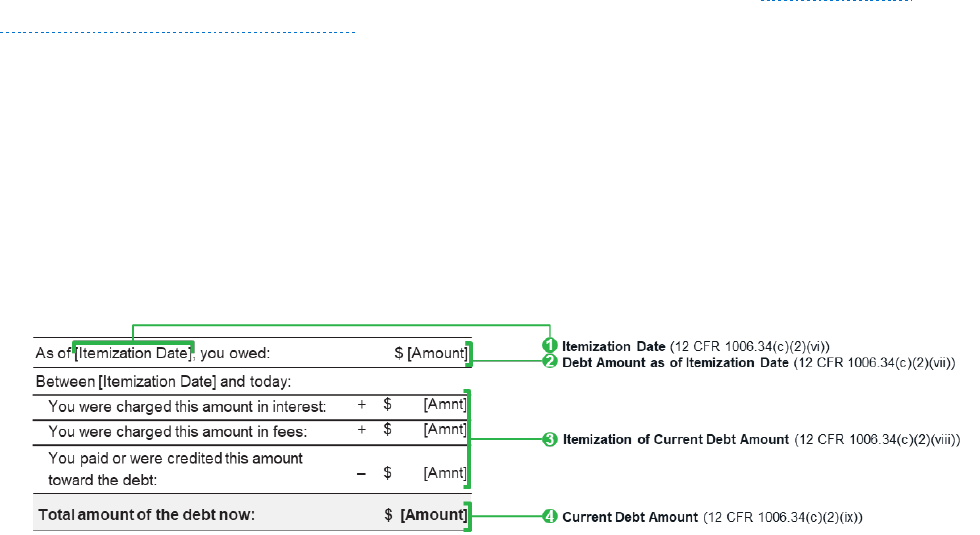

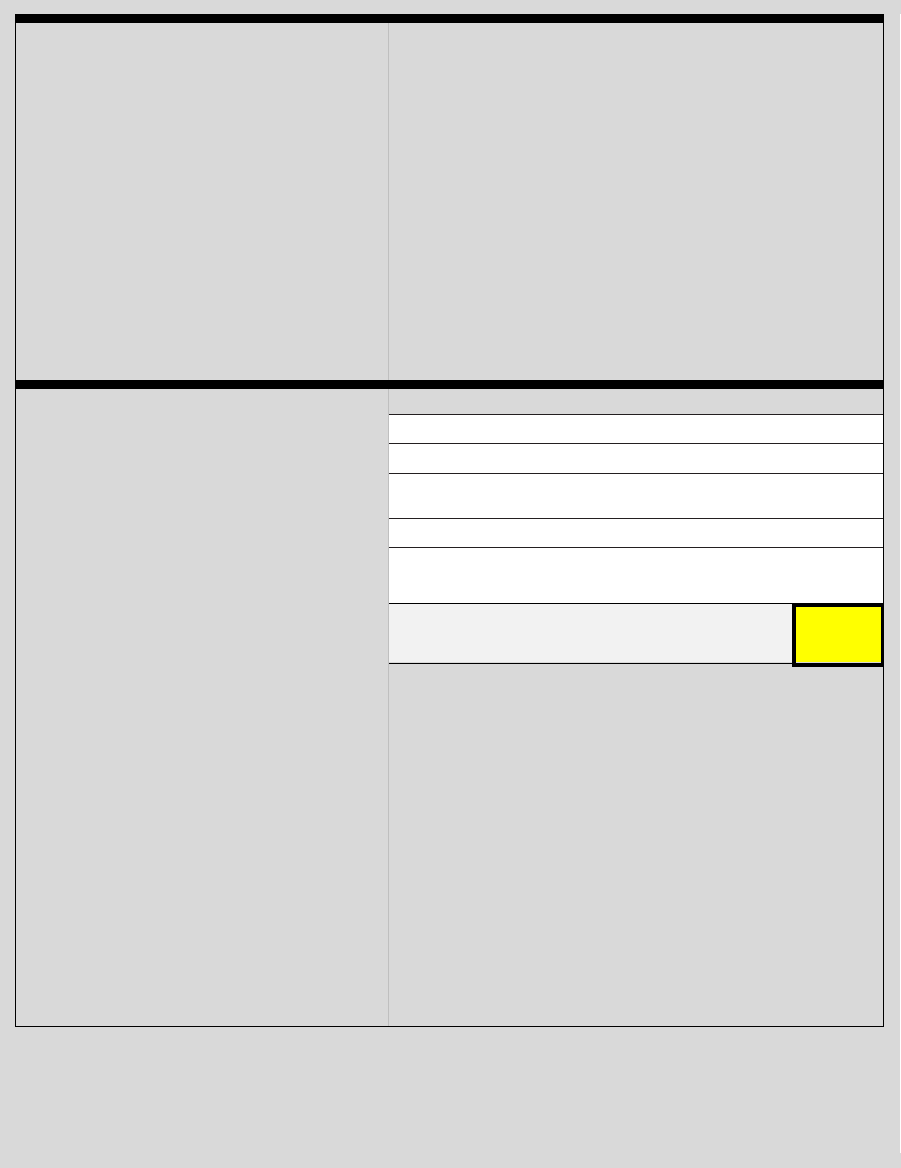

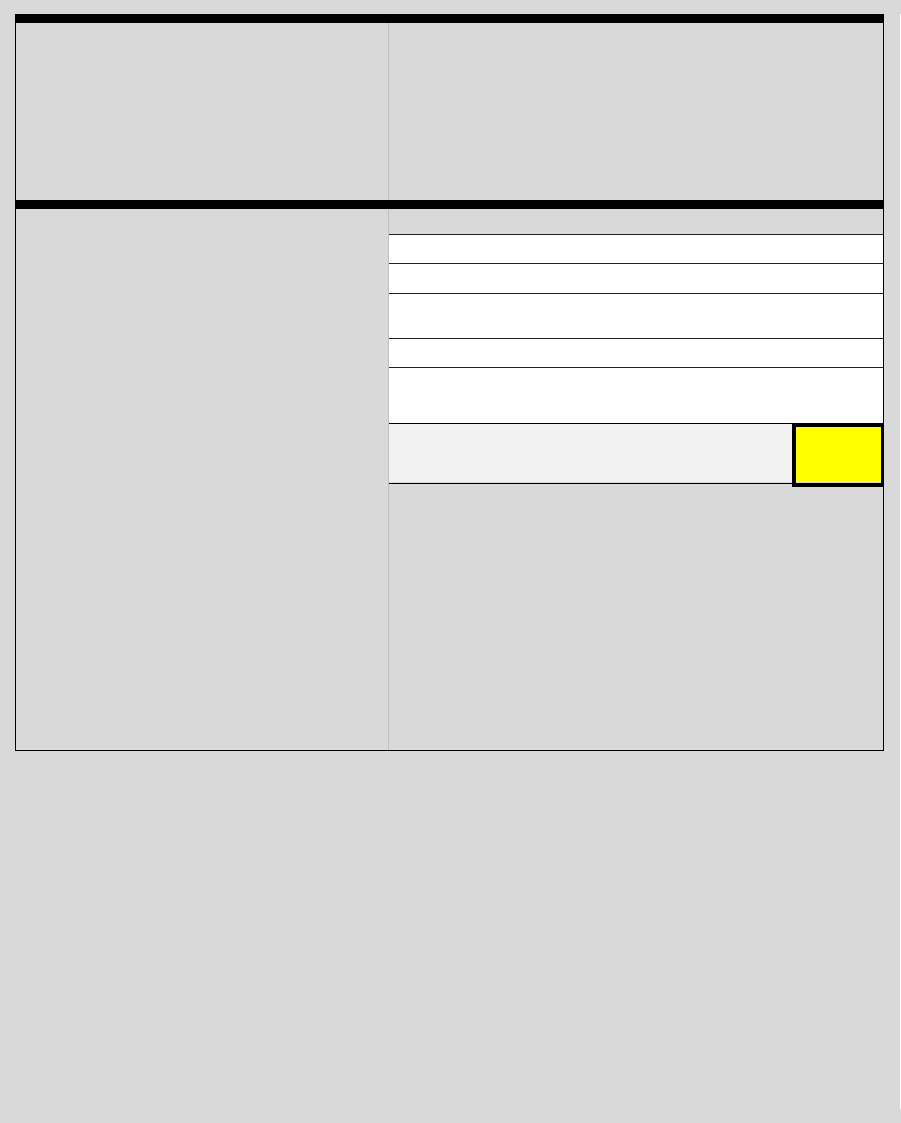

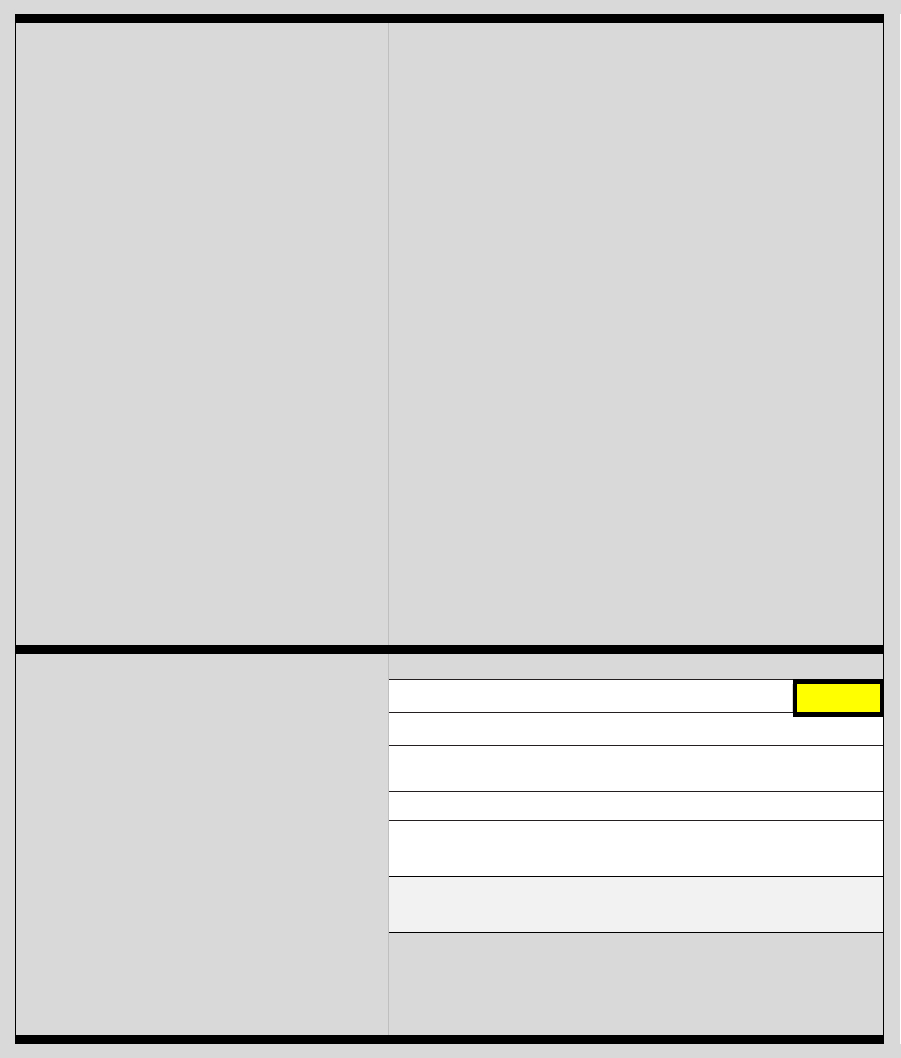

Figure 1 provides an annotated version of the Itemization Table showing where this information is

disclosed on the model validation notice.

FIGURE 1: ANNOTATED MODEL VALIDATION NOTICE ITEMIZATION TABLE

One way a debt collector using the model validation notice may, but is not required to, complete

the Itemization Table to disclose this information is to use the following four steps:

1. Select the itemization date;

2. Determine the amount of the debt as of the itemization date;

3. Determine the Itemized Amounts since the itemization date; and

4. Determine the current amount of the debt.

These steps are discussed in more detail below.

Steps to Complete the Itemization Table

Step 1: Select the itemization date

Generally, a debt collector will begin the process of completing the Itemization Table by selecting

the itemization date for the debt. Although the Rule does not require a debt collector to start with

5 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

this step, a debt collector likely will need to do so because two of the other three components of the

Itemization Table (i.e., the debt amount as of the itemization date and the itemization of the

current debt amount) and other validation information outside the Itemization Table

5

are directly

tied to the itemization date.

To select the itemization date for the Itemization Table, a debt collector must select one of the

following reference dates: 1) the last creditor statement date; 2) the charge-off date; 3) the last

payment date; 4) the transaction date; or 5) the judgment date. These events may occur at any

point in the history of the debt, and are not necessarily close to the date the validation information

is provided. Depending on the facts and circumstances, a debt may or may not have all five

reference dates. 12 CFR 1006.34(b)(3); 1006.34(c)(2)(vi).

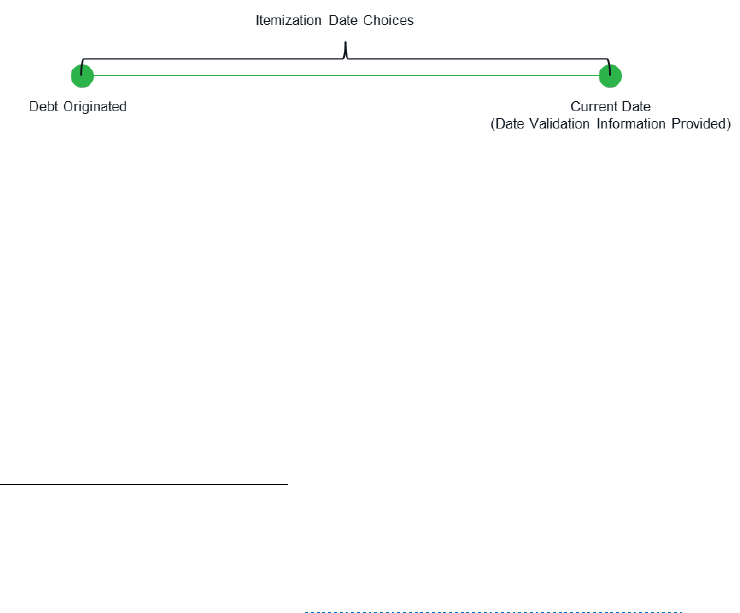

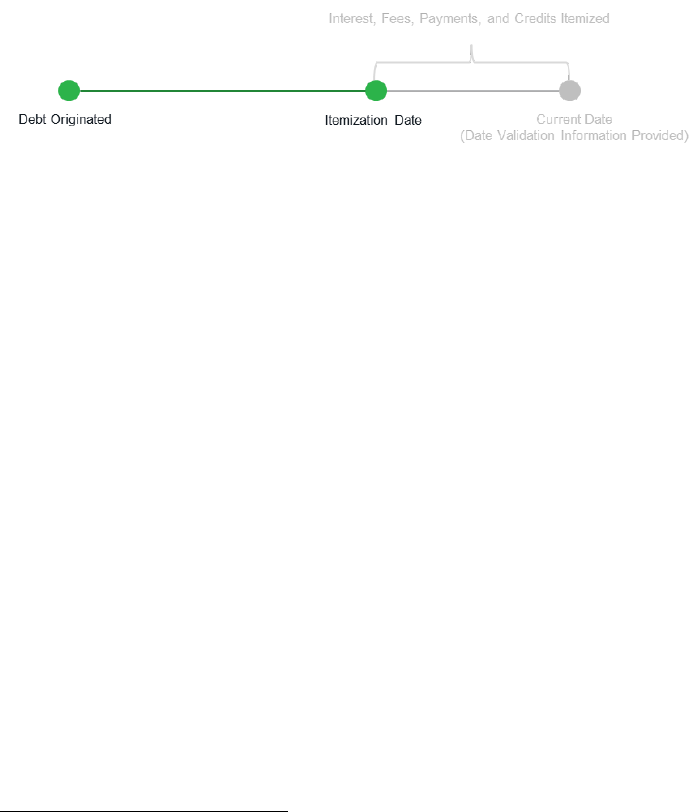

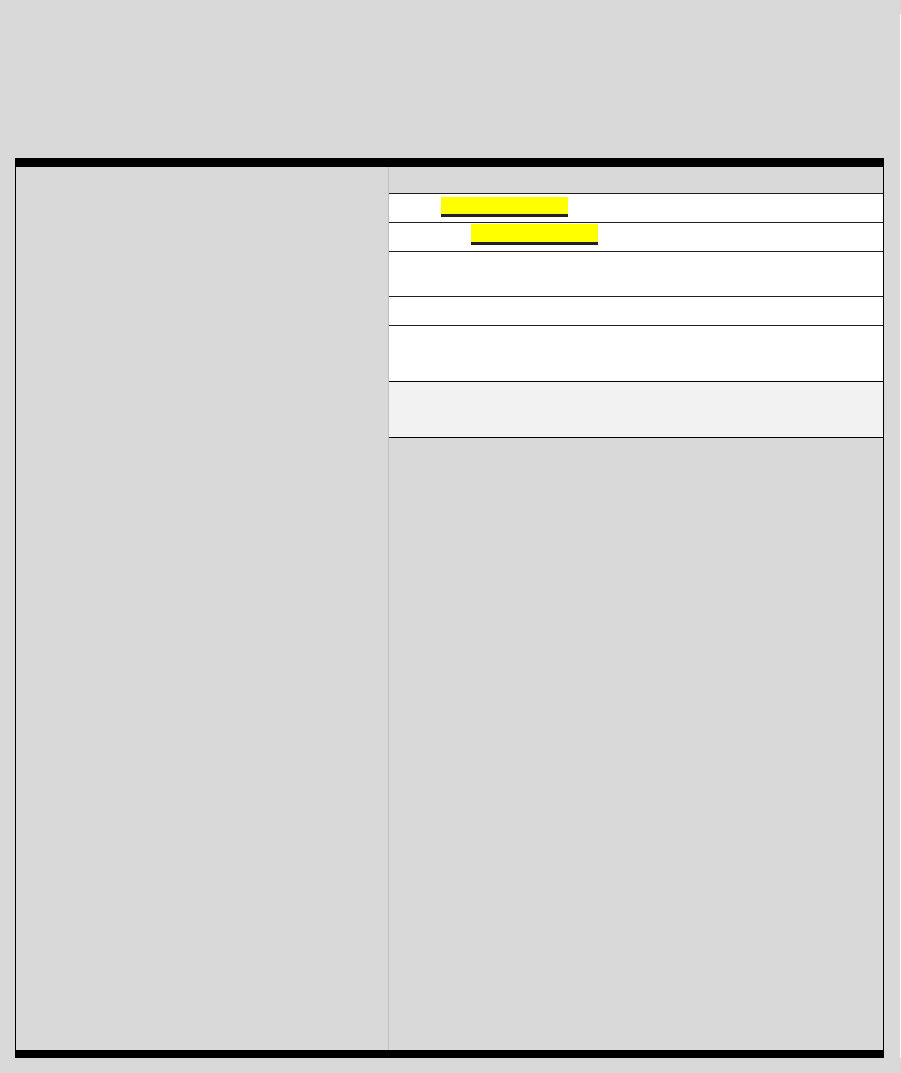

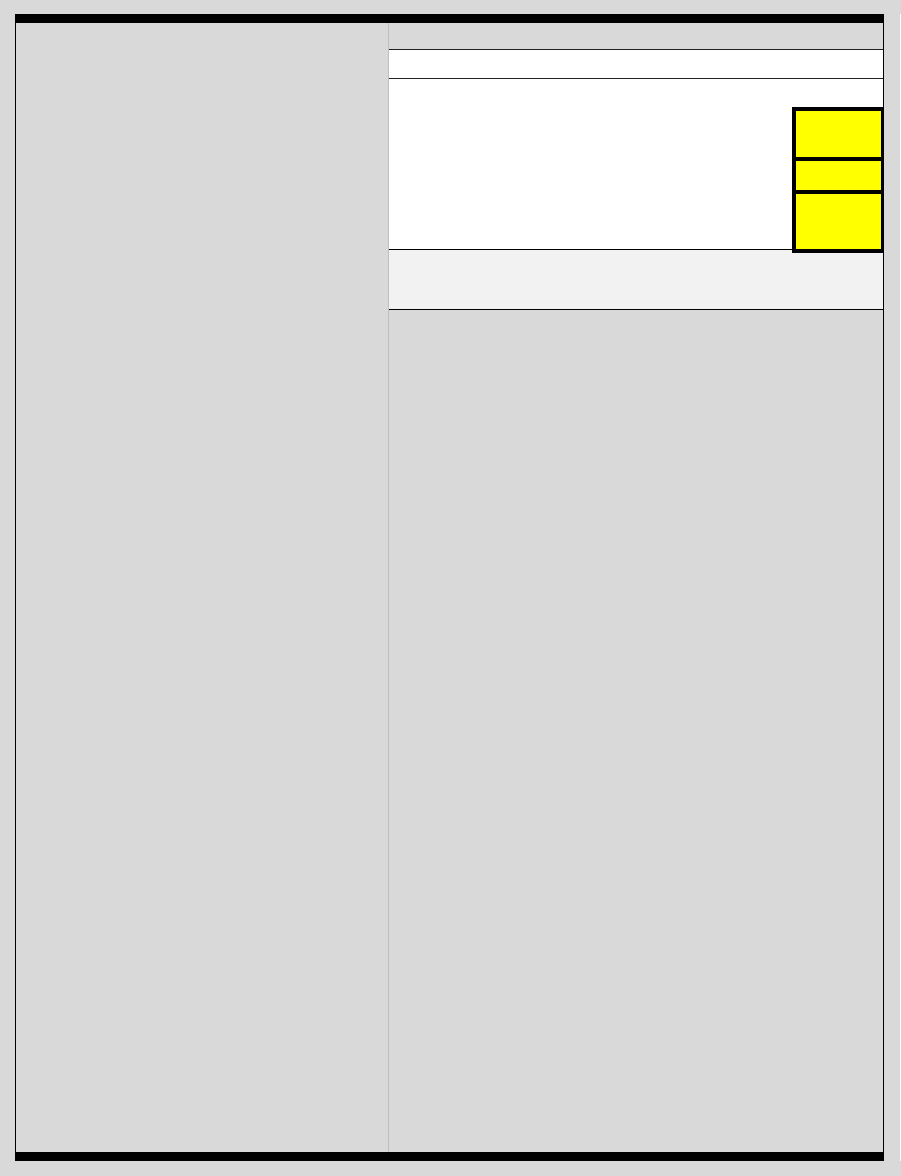

FIGURE 2: TIME PERIOD DURING WHICH THE ITEMIZATION DATE MAY OCCUR

6

Once a debt collector uses an itemization date in a communication providing the itemization

information to the consumer, the debt collector must consistently use that date when a required

disclosure for that consumer is based on the itemization date. For example, if a debt collector uses

the last statement date to determine and disclose the amount of the debt as of the itemization date

(Step 2), the debt collector may not use the charge-off date to itemize the current amount of the

debt in the validation notice (Step 4). Comment 1006.34(b)(3)-1. However, a subsequent debt

5

For example, a debt collector is required to disclose the account number, if any, as of the itemization date and the

creditor information as of the itemization date, if applicable, although this information is not included in the

Itemization Table. 12 CFR 1006.34(c)(2)(iii) and 34(c)(2)(iv). More information about this validation information

can be found in Section 12.1.1 of the Debt Collection Small Entity Compliance Guide

.

6

Depending on which reference date the debt collector selects, the itemization date may fall anywhere between the

origination date and the date the validation information is provided. For ease of reference, the remaining illustrations

in this guidance document assume the itemization date occurs roughly midway between origination and the date the

validation notice is provided.

6 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

collector need not use the same itemization date as a prior debt collector. Comment

1006.34(b)(3)-2.

Details about the reference dates that may serve as the itemization date are discussed below.

LAST STATEMENT DATE

The last statement date is the date of the last written account statement, invoice, or periodic

statement (including, but not limited to, any statements required by law) provided to the

consumer by a creditor. 12 CFR 1006.34(b)(3)(i). A debt collector who selects the last

statement date as the itemization date must identify the date of the last written statement or

invoice provided to the consumer by a creditor.

For purposes of determining the itemization date, a statement qualifies as the last statement

only if it was provided by the creditor or a third party acting on the creditor’s behalf, such as a

creditor’s service provider. A statement or invoice provided by a debt collector is not a last

statement for purposes of the itemization date disclosed in the Itemization Table, unless the

debt collector is also a creditor.

7

Comment 1006.34(b)(3)(i)-1. For example, assume a

mortgage servicer is also a “debt collector” under the Rule. Assume also that this debt collector

may, but chooses not to, use the special rule for certain residential mortgage debt, and instead

discloses the Itemization Table in the validation notice. Under these circumstances, if the debt

collector selects the last statement date as the itemization date, the debt collector would need to

determine the date of the last statement provided by a creditor (or a prior mortgage servicer

acting on the creditor’s behalf that was not also a “debt collector” under the Rule). The debt

collector could not use the date of a periodic statement that it or any other debt collector

provided to the consumer, unless that debt collector was also a creditor.

Common statement types that may be the last statement provided to the consumer by a creditor

include periodic billing statements, a written statement provided on behalf of a creditor during

7

Note, however, if a debt collector chooses to use the special rule for certain residential mortgages, discussed in

footnotes 3 and 4 above, to disclose the itemization date-dependent information when providing the validation notice,

the debt collector uses the date of the most recent periodic statement. That periodic statement may be one that the

debt collector (or a previous debt collector) provided the consumer, even if the debt collector (or a previous debt

collector) is not a creditor. For more information on the special rule for certain residential mortgage debt, see the

Debt Collection Rule FAQs, Validation Information: Residential Mortgage Debt Questions

.

7 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

default judgment proceedings, or a final invoice from the creditor. 12 CFR 1006.34(b)(3)(i);

1006.34(c)(5).

CHARGE-OFF DATE

The charge-off date is the date the debt was charged off. 12 CFR 1006.34(b)(3)(ii). The Rule

does not limit the charge-off date to a charge off made by the creditor. For example, for

residential mortgage loans, the charge-off date may be the date that either the creditor or

servicer of the mortgage loan charged off the debt. 12 CFR 1006.34(b)(3)(ii).

LAST PAYMENT DATE

The last payment date is the date the last payment was applied to the debt. 12 CFR

1006.34(b)(3)(iii). If selecting the last payment date as the itemization date, the debt collector

must identify the last payment applied to the account and use that date.

The Rule does not limit the last payment only to payments that count as periodic payments or

full payments under the terms of the contract. The last payment used to identify the last

payment date therefore may be a periodic payment, or it may be a non-periodic payment, a

partial payment, or a non-conforming payment. For example, a payment the consumer made

as part of loss mitigation or as an attempt to reinstate the account may be the last payment for

purposes of determining the last payment date.

The last payment used to identify the last payment date need not be from the consumer. The

last payment may also be one made by a third party. For example, the last payment may be a

payment from an auto repossession agent, such as auction proceeds, that was applied to the

debt, or it may be a payment from an insurance company that was applied to the debt, so long

as those were the last payments on the account. Comment 1006.34(b)(3)(iii)-1. Other

examples of last payments made by third parties may include the application of the proceeds

from a real estate sale to the account.

The Rule does not limit the last payment only to payments applied to the account by a creditor.

For example, payments applied by a debt collector or third-party payment processor may count.

TRANSACTION DATE

The transaction date is the date of the transaction that gave rise to the debt, i.e., the date that

the good or service that gave rise to the debt was provided or made available to the consumer.

12 CFR 1006.34(b)(3)(iv); Comment 1006.34(b)(3)(iv)-1. For example, the transaction date for

a debt arising from a medical procedure may be the date the medical procedure was performed,

8 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

and the transaction date for a consumer’s gym membership may be the date the membership

contract was executed. Comment 1006.34(b)(3)(iv)-1. For a residential mortgage, the

transaction date may be the date the mortgage was originated, but is not, for example, the date

of a mortgage servicing transfer.

In some cases, a debt may have more than one transaction date. If a debt has more than one

transaction date, a debt collector may use any of those dates as the transaction date for

purposes of the itemization date. For example, if a consumer enters into a contract on one date

and the creditor performs the contracted service on another date, the debt collector may select

either date as the transaction date. Comment 1006.34(b)(3)(iv)-1.

Additionally, for some debts, not only are there separate dates for the agreement to provide

services and the provision of those services, but those services may be provided on multiple

days. For example, for a medical debt where multiple procedures giving rise to the debt were

provided by the same creditor, depending on the facts and circumstances, a debt collector may

select any of the dates the procedures were performed as the transaction date.

If a debt has multiple transaction dates, whichever date the debt collector selects must be used

consistently in the validation notice. Comment 1006.34(b)(3)(iv)-1.

JUDGMENT DATE

The judgment date is the date of any final court judgment that determines the amount of the

debt owed by the consumer. 12 CFR 1006.34(b)(3)(v). In the case of a final judgment renewal,

depending on the facts and circumstances, the final judgment renewal may be the judgment

date.

Once a debt collector selects the itemization date for the debt, the debt collector can then

determine the other components of the Itemization Table.

Step 2: Determine the amount of the debt as of the itemization date

Using the itemization date selected under Step 1, the debt collector next determines the amount of

the debt as of the itemization date. 12 CFR 1006.34(c)(2)(vii). For example, depending on the

facts and circumstances, the amount of the debt as of the itemization date may be the amount of

the debt that is required to bring the account current as of that date or the total outstanding debt

as of that date.

9 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

The amount must include any interest, fees, or other charges owed, less any payments or credits

applied, by the itemization date. Comment 1006.34(c)(2)(vii)-1.

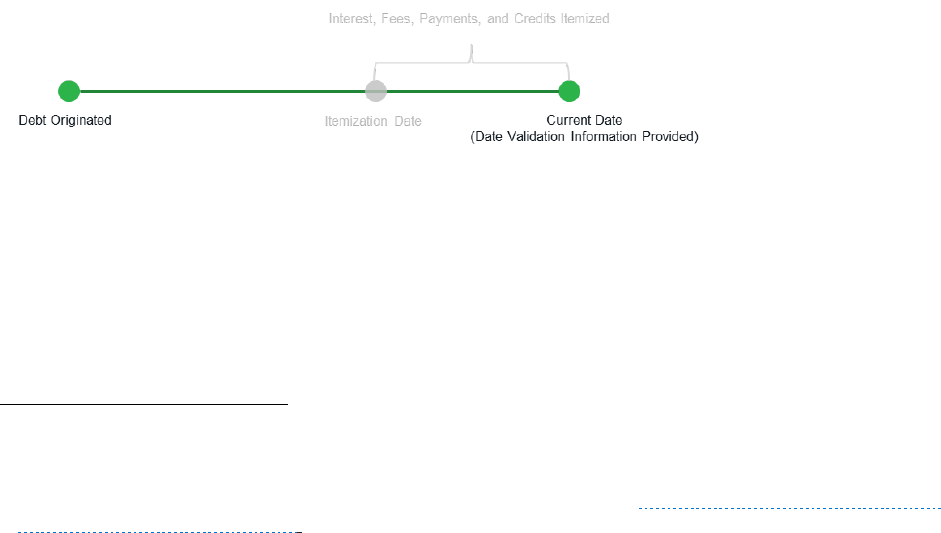

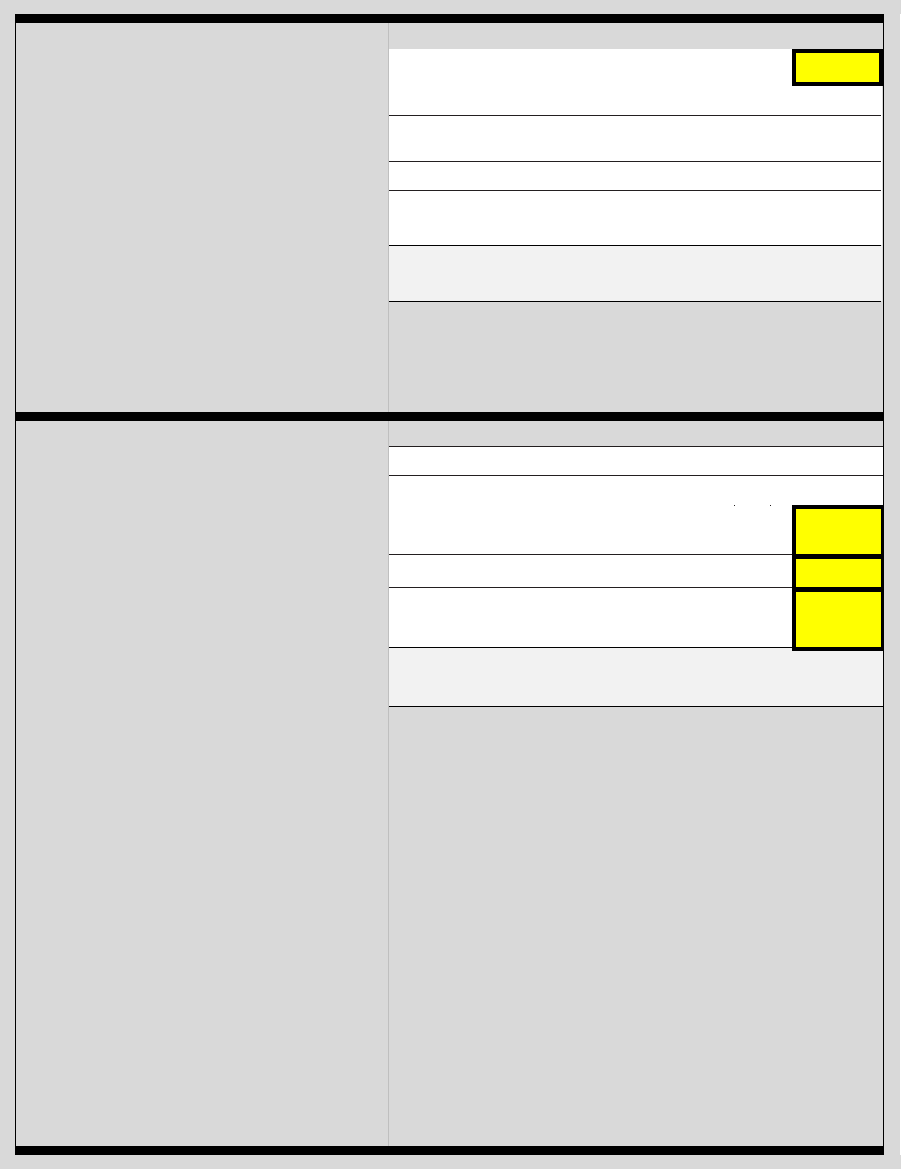

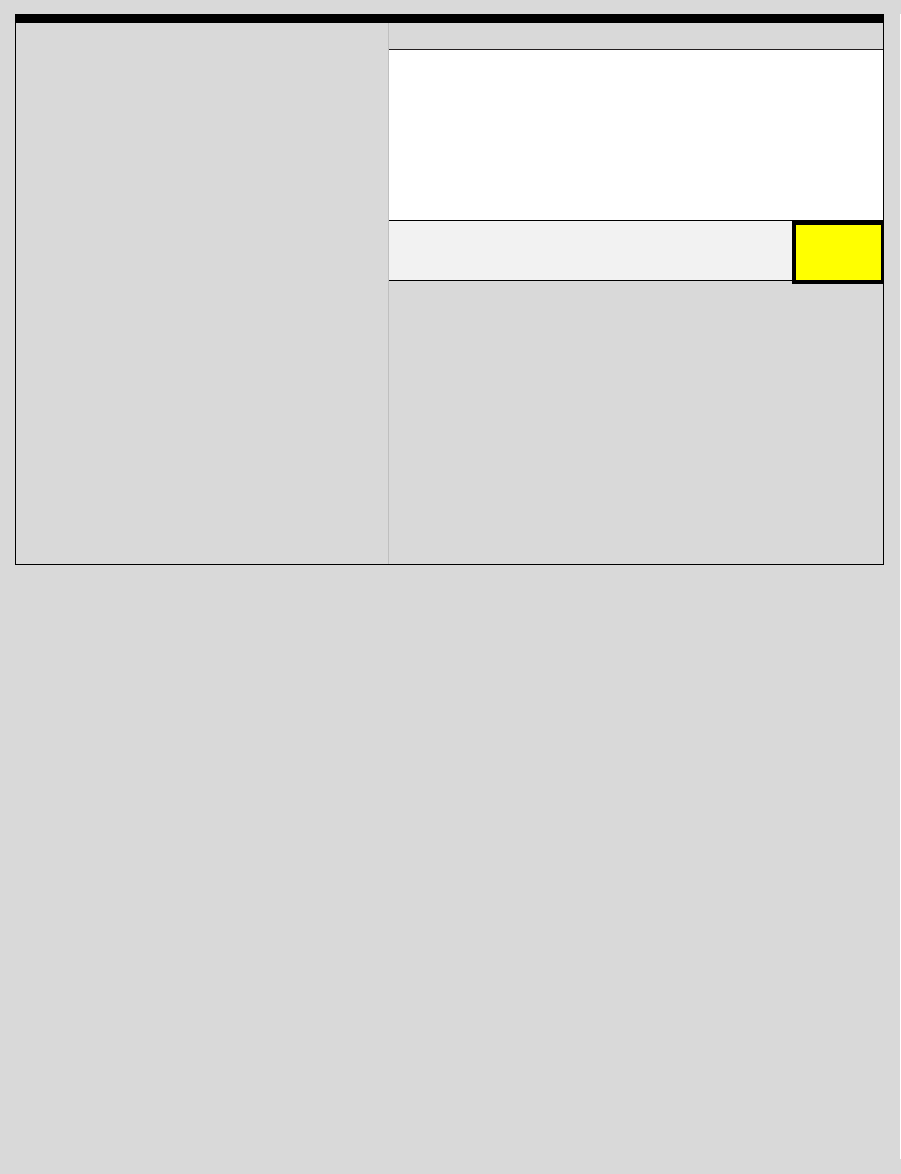

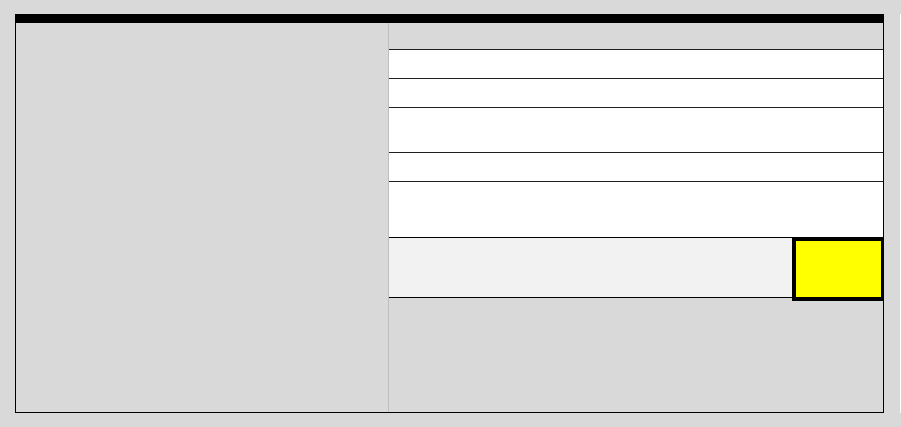

FIGURE 3: TIME PERIOD ILLUSTRATION FOR THE DEBT AMOUNT AS OF THE ITEMIZATION DATE

Figure 3 illustrates the relevant time period for amount of the debt as of the itemization date. For

example, if a debt collector is using the transaction date as the itemization date and selects the

latest of multiple permissible dates, then any amounts applied to the account as of that date are

reflected in this disclosure determined in Step 2.

The amount is disclosed in the first row of the Itemization Table.

Step 3: Determine the Itemized Amounts since the itemization date

8

Next, a debt collector itemizes the current amount of the debt, disclosing any interest, fees,

payments, and credits (the Itemized Amounts) between the itemization date and the date the

validation information is provided. 12 CFR 1006.34(c)(2)(viii); Comment 1006.34(c)(2)(ix)-1. For

ease of reference, this guidance document refers to the time period between the itemization date

and the date the validation information is provided as the “Itemization Period.”

8

Even if using the model validation notice, a debt collector is permitted under the Rule to provide the Itemized

Amounts discussed in Step 3 on a separate page(s) instead of in the Itemization Table. If the debt collector does so,

however, the debt collector must include the separate page(s) in the same communication with the validation notice

and include on the validation notice, where the itemization information would have appeared, a statement referring to

that separate page(s). 12 CFR 1006.34(c)(2)(viii); Comment 1006.34(c)(2)(viii)-3. Note that the information

provided on the separate page does not receive the safe harbor for the validation information content and format

requirements. 12 CFR 1006.34(d)(2); see also 12 CFR 1006.34(c) and 34(d)(1).

10 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

FIGURE 4: ITEMIZATION PERIOD ILLUSTRATION

The Rule does not define interest, fees, payments, or credits for purposes of determining the

Itemized Amounts. As such, the Rule does not specify a particular accrual method that debt

collectors must use to calculate interest, but the disclosed interest amount must be accurate. For

example, depending on the facts and circumstances, a debt collector may use the interest accrual

method (e.g., monthly, simple interest, average daily balance method) in any underlying debt

agreement, or may use a method that is otherwise customarily used for the debt.

The Rule requires disclosure of any Itemized Amounts applied to the account during the

Itemization Period, regardless of the source. For example, a third-party payment or insurance

adjustment may be disclosed either as a “payment” or a “credit” in the itemization.

9

An interest, fee, payment, or credit amount applied to the account during the Itemization Period,

but that is returned or reversed during that same period, may be omitted from the Itemization

Table. For example, a payment made during the Itemization Period that was also returned during

the Itemization Period may be omitted from the Itemized Amounts, provided that the payment

and the return offset each other, and the other amounts are disclosed accurately.

There may be circumstances in which an amount cannot be accurately categorized as interest or a

fee, payment, or credit. In such a case, a debt collector who accurately itemizes only the interest,

fees, payments, and credits complies with the Rule even if there are amounts included in the

“current amount of the debt” disclosure (Step 4) that are not included in the itemization of the

debt.

10

The Rule does not require that the amount of the debt as of the itemization date, plus or

9

Note that, in the Itemization Table, these two fields are disclosed as a single amount.

10

A debt collector could choose to add a field to the itemization for amounts that cannot accurately be characterized as

an Itemized Amount, as long as the amount is accurately described and not combined with the Itemized Amounts.

11 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

minus the Itemized Amounts, equal the “current amount of the debt,” even if the debt collector

uses the Itemization Table. For example, if the creditor provided another service to the consumer

during the Itemization Period, the debt collector may, depending on the facts and circumstances,

not need to disclose that service charge amount in the Itemized Amounts. However, if the service

charge is part of the debt being collected, the debt collector must still include the amount in the

“current amount of the debt” (Step 4).

If no additional amounts have accrued since the itemization date, a debt collector may include a

“0” or “none,” or may state that no interest, fees, payments, or credits have been assessed or

applied to the debt. Comment 1006.34(c)(2)(viii)-1.

Step 4: Determine the current debt amount

Finally, the debt collector must disclose the amount of the debt as of when the validation

information is provided. 12 CFR 1006.34(c)(2)(ix). This amount includes the amount of the debt

as of the itemization date from Step 2, as well as the Itemized Amounts from Step 3, and, if

applicable, any amounts from the Itemization Period that could not be accurately categorized as an

Itemized Amount (i.e., as interest or a fee, payment, or credit).

FIGURE 5: TIME PERIOD ILLUSTRATION FOR THE CURRENT AMOUNT OF THE DEBT

For example, depending on the facts and circumstances, the current amount of the debt may be

the amount of the debt that is required to bring the account current as of when the validation

information is provided or the total outstanding debt when the validation information is provided.

The Rule does state that, for residential mortgage debt subject to the periodic statement

However, if the validation notice with the added information is not substantially similar to the model validation

notice, then the safe harbor does not apply with respect to the entirety of the validation notice. For more discussion

on the safe harbor and making changes to the model validation notice, see the

Debt Collection Rule FAQs, Validation

Information Questions 2 through 4.

12 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

requirements under Regulation Z, the debt collector may provide the current amount of the debt

by providing the consumer the total balance of the outstanding mortgage, including principal,

interest, fees, and other charges. Comment 1006.34(c)(2)(ix)-1.

Example Itemization Tables

Each of the examples below describes the collection of one type of debt and illustrates how a debt

collector could complete the Itemization Table assuming the facts described in the example. The

examples are only illustrations of the concepts discussed above and are not necessarily the only

way to comply with the Rule. They are not meant to be examples of compliance with other rules.

Example 1: Credit card debt

For this debt, assume the following timeline of events:

March 21, 2011: The consumer opened a credit card with Ficus Bank, a creditor.

September 1, 2021: Ficus Bank applied the last payment made by the

consumer. After September 1

st

, no payments were received for, or applied to, the

account. The account went into default.

March 15, 2022: Ficus Bank provided the last monthly billing statement before

the account was charged off.

March 30, 2022: Ficus Bank charged off the debt. As of March 5

th

, including

pre-charge off interest and fees, the consumer owed $10,000.

April 15, 2022: Ficus Bank determined an amount of $100 the consumer

previously disputed was correctly charged and added the transaction back to the

debt.

May 1, 2022: Ficus Bank assigned the debt to ABC Financial, Inc., a debt

collector, for collection.

May 30, 2022: ABC Financial, Inc., provided the validation notice.

13 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Also assume that, since the charge-off date (March 30, 2022), the account did not

accumulate any interest or fees.

Based on these facts, ABC Financial, Inc., could disclose the Itemization Table by

applying the four steps discussed above as follows:

Step 1: Select an itemization

date.

This example uses the charge-off

date (March 30, 2022).

Other available reference dates in

this example include:

Transaction date: March 21,

2011, the date the account was

opened.

Last payment date: September

1, 2021, the date the last

payment was applied to the

account.

Last statement date: March 15,

2022, the date of the last

statement sent by the creditor.

Note: In this example, there is no

judgment date.

As of March 30, 2022, you owed:

$

Between March 30, 2022 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

14 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 2: Determine the amount

of the debt as of the

itemization date.

Enter the account balance as of the

itemization date selected in Step 1

(March 30, 2022).

As of March 30, 2022, you owed:

$

10,000.00

Between March 30, 2022 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

Step 3: Determine the Itemized

Amounts since the itemization

date.

Enter the interest and fees charged,

as well as the payments and credits

applied, to the account during the

Itemization Period (i.e., between

the itemization date (March 30,

2022) and the date the validation

information is provided (May 30,

2022)).

Interest: No interest was

charged during the Itemization

Period. This field must still be

disclosed. In this example, the

field is disclosed as “0,” as

permitted by the Rule.

Fees: No fees were charged

during the Itemization Period.

This field must still be

disclosed. In this example, the

As of March 30, 2022, you owed:

$

10,000.00

Between March 30, 2022 and today:

You were charged this amount in

interest:

+

$

0

You were charged this amount in fees: +

$

0

You paid or were credited this

amount toward the debt:

–

$

0

Total amount of the debt now:

$

15 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

field is disclosed as “0,” as

permitted by the Rule.

Payments and Credits: No

payments were made and no

credits were applied during the

Itemization Period. This field

must still be disclosed. In this

example, the field is disclosed

as “0,” as permitted by the Rule.

Step 4: Determine the current

debt amount.

Enter the current account balance

as of the date the validation

information is provided (May 30,

2022).

Because of the circumstances, ABC

Financial, Inc., did not include the

post-dispute amount ($100) in the

Itemized Amounts. However, ABC

Financial, Inc., did include the

post-disputed amount in the

current amount of the debt.

This is the completed Itemization

Table ABC Financial, Inc., included

in the validation notice.

As of March 30, 2022, you owed:

$

10,000.00

Between March 30, 2022 and today:

You were charged this amount in

interest:

+

$

0

You were charged this amount in fees: +

$

0

You paid or were credited this

amount toward the debt:

–

$

0

Total amount of the debt now:

$

10,100.

00

16 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Example 2: Residential mortgage debt

For this loan, assume the following timeline of events:

January 5, 2013: The consumer originated a $100,000 mortgage loan with

Ficus Bank.

February 2013 - January 2022: The consumer made mortgage payments as

due. During that time, Ficus Bank transferred servicing to Ficus Mortgage

Company, a mortgage servicer.

February 5, 2022: Ficus Mortgage Company applied a partial payment from the

consumer to the account. This was the last payment applied to the account. Ficus

Mortgage Company later determined the consumer was in default.

August 5, 2022: Ficus Mortgage Company sent its last Regulation Z-required

periodic statement to the consumer before servicing of the account was

transferred to another servicer. As of August 5

th

, the consumer’s account balance

was $75,234.56.

August 15, 2022: Ficus Mortgage Company transferred servicing of the

defaulted account to a different mortgage servicer, ABC Financial, Inc. ABC

Financial, Inc., is also a “debt collector” under the Rule.

September 5, 2022: ABC Financial, Inc., sent its first Regulation Z-required

periodic statement to the consumer.

September 6, 2022: ABC Financial, Inc., provided the validation notice.

Also assume that, since the date of the last statement provided by the creditor (August 5,

2022), the account accrued $260 in interest and $75 in fees (all permitted by the

underlying mortgage contract signed by the consumer). The fees were comprised of $25

in late fees and $50 in property inspection fees.

If ABC Financial, Inc., chooses to use the model validation notice, it has two options: 1) it

may fully complete the Itemization Table, or 2) it may use the special rule for certain

residential mortgages.

17 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Option 1: Fully complete the Itemization Table

Based on these facts, ABC Financial, Inc., could disclose the Itemization Table by

applying the four steps discussed above as follows:

Step 1: Select an itemization

date.

This example uses the last

statement date (August 5, 2022).

Remember, the last statement date

is not September 5, 2022, the date

of the periodic statement sent by

ABC Financial, Inc. That statement

was provided by a debt collector

who was not also a creditor.

Other available reference dates in

this example include:

Transaction date: January 1,

2013, the date the mortgage

was originated.

Last payment date: February 5,

2022, the date the consumer’s

partial payment was applied to

the account.

Note: In this example, there is no charge-

off date or judgment date.

As of August 5, 2022, you owed:

$

Between August 5, 2022 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

18 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 2: Determine the amount

of the debt as of the

itemization date.

Enter the amount of the debt as of

the itemization date selected in

Step 1 (August 5, 2022).

ABC Financial, Inc., discloses the

total outstanding debt, as permitted

by the Rule.

As of August 5, 2022, you owed:

$

75,234.56

Between August 5, 2022 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

Step 3: Determine the Itemized

Amounts since the itemization

date.

Enter the interest and fees charged,

as well as the payments and credits

applied, to the account during the

Itemization Period (i.e., between

the itemization date (August 5,

2022) and the date the validation

information is provided (September

6, 2022)).

Interest: $260 for the

Itemization Period.

Fees: $75 for the Itemization

Period. $25 in late fees and

$50 in property inspection fees.

Payments and Credits: No

payments were made and no

credits were applied during the

As of August 5, 2022, you owed:

$

75,234.56

Between August 5, 2022 and today:

You were charged this amount in

interest:

+

$

260.00

You were charged this amount in fees: +

$

75

.00

You paid or were credited this

amount toward the debt:

–

$

0

Total amount of the debt now:

$

19 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Itemization Period. This field

must still be disclosed. In this

example, the field is disclosed

as “0,” as permitted by the Rule.

Step 4: Determine the current

debt amount.

Enter the amount of the debt as of

the date the validation information

is provided (September 6, 2022).

ABC Financial, Inc., discloses the

total balance of the outstanding

mortgage, including principal,

interest, fees, and other charges, as

permitted by the Rule.

This is the completed Itemization

Table ABC Financial, Inc., included

in the validation notice.

As of August 5, 2022, you owed:

$

74,234.56

Between August 5, 2022 and today:

You were charged this amount in

interest:

+

$

260

.00

You were charged this amount in fees: +

$

75

.00

You paid or were credited this

amount toward the debt:

–

$

0

Total amount of the debt now:

$

74,569

.56

Option 2: Use the Special Rule for Certain Residential Mortgage Debt

Based on these facts, ABC Financial, Inc., would provide, in the same

communication with the validation notice, a copy of the most recent periodic

statement required by Regulation Z, 12 CFR 1026.41. When doing so, ABC

Financial, Inc., could disclose the Itemization Table by applying the four steps

discussed above as follows:

20 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 1: Select an itemization date.

Because ABC Financial, Inc., is using the special rule for certain residential mortgage

debt

11

, ABC Financial, Inc., need not disclose an itemization date on the validation

notice. However, ABC Financial, Inc., still needs to determine an itemization date to

disclose the other itemization date-dependent validation information.

Under the special rule for certain residential mortgage debt, ABC Financial, Inc., uses

the date of the most recent periodic statement provided under Regulation Z

(September 5, 2022) as the itemization date, even though that periodic statement was

provided by a debt collector who was not also a creditor.

Step 2: Determine the amount of the debt as of the itemization date.

ABC Financial, Inc., need not determine or disclose this amount on the validation

notice.

Instead, ABC Financial, Inc., discloses a statement on the validation notice referring

the consumer to the enclosed periodic statement. 12 CFR 1006.34(c)(5)(ii).

Step 3: Determine the Itemized Amounts since the itemization date.

ABC Financial, Inc., need not determine or disclose this itemization on the validation

notice.

Instead, ABC Financial, Inc., discloses a statement on the validation notice referring

the consumer to the enclosed periodic statement. 12 CFR 1006.34(c)(5)(ii).

11

See the Debt Collection Rule FAQs, Validation Information: Residential Mortgage Debt Questions and footnotes 3, 4,

and 7 above for more information on the special rule for certain residential mortgage debt. 12 CFR 1006.34(c)(5).

21 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 4: Determine the current

debt amount.

Enter the amount of the debt as of

the date the validation information

is provided (September 6, 2022).

ABC Financial, Inc., discloses the

total balance of the outstanding

mortgage, including principal,

interest, fees, and other charges, as

permitted by the Rule.

This is the completed Itemization

Table ABC Financial, Inc., included

in the validation notice.

See the enclosed periodic statement for an itemization

of the debt.

Total amount of the debt now:

$

74,569

.56

Example 3: Medical debt

ABC Financial, Inc., a debt collector, is collecting on a past-due consolidated medical debt

for multiple procedures related to a consumer’s week-long hospital stay. For this debt,

assume the following timeline of events:

June 25, 2021 - July 2, 2021: The consumer was admitted to Regional

Hospital for a week. The consumer was admitted on June 25, 2021, and had

multiple procedures over the week, including on June 26

th

, June 28

th

, July 1

st,

and

July 2

nd

. On July 2, 2021, the consumer was discharged.

August 15, 2021: The consumer was seen for a follow-up appointment related to

the prior hospital procedure. As of August 15

th

, the total medical debt was

$40,000.

September 1, 2021: The consumer’s health insurance required an adjustment of

$3,000 of the amount charged for a procedure.

22 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

October 1, 2021 - December 1, 2021: The consumer’s health insurance

company made several payments totaling $30,000, the last of which was applied

to the account on December 1

st

. The insurance company notified the consumer

and the hospital that the consumer was responsible for the remainder of the debt.

January 1, 2022 - May 5, 2022: Regional Hospital sent account statements to

the consumer. On May 5

th

, Regional Hospital sent a final invoice to the consumer

stating the outstanding balance.

June 1, 2022: Because the account was in default, Regional Hospital charged off

the debt.

August 1, 2022: Regional Hospital placed the debt with ABC Financial, Inc., a

debt collector, for collection.

September 15, 2022: ABC Financial, Inc., provided the validation notice.

Also assume that, since the date of the last procedure (August 15, 2021), the account did

not accumulate any interest or fees.

Based on these facts, ABC Financial, Inc., could disclose the Itemization Table by

applying the four steps discussed above as follows:

Step 1: Select an itemization

date.

This example uses a transaction

date (August 15, 2021). This is the

date of the last appointment related

to the hospital procedure for the

debt.

Other available reference dates in

this example include:

Transaction date: Alternative

transaction dates for this fact

pattern may include June 25,

As of August 15, 2021, you owed:

$

Between August 15, 2021 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

23 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

2021 (date of admission); June

26, June 28, July 1, or July 2,

2021 (dates of procedures); or

July 2, 2021 (date of discharge).

Last payment date: December

1, 2021, the date the last

payment was applied to the

account. This payment was

made by the insurance

company.

Last statement date: May 5,

2022, the date of the last

statement sent by the creditor.

Charge-off date: June 1, 2022.

Note: In this example, there is no

judgment date.

Step 2: Determine the amount

of the debt as of the

itemization date.

Enter the account balance as of the

itemization date selected in Step 1

(August 15, 2021).

As of August 15, 2021, you owed:

$

40,000.00

Between August 15, 2021 and today:

You were charged this amount in

interest:

+

$

You were charged this amount in fees: +

$

You paid or were credited this

amount toward the debt:

–

$

Total amount of the debt now:

$

24 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 3: Determine the Itemized

Amounts since the itemization

date.

Enter the interest and fees charged,

as well as the payments and credits

applied, to the account during the

Itemization Period (i.e., between

the itemization date (August 15,

2021) and the date the validation

information is provided (September

15, 2022)).

Interest: No interest was

charged during the Itemization

Period. This field must still be

disclosed. In this example, the

field is disclosed as “0,” as

permitted by the Rule.

Fees: No fees were charged

during the Itemization Period.

This field must still be

disclosed. In this example, the

field is disclosed as “0,” as

permitted by the Rule.

Payments and Credits:

$33,000 for the Itemization

Period. The health insurance

company made $30,000 in

payments. Additionally, an

insurance adjustment of

$3,000 occurred during this

time period.

As of August 15, 2021, you owed:

$

40,000.00

Between August 15, 2021 and today:

You were charged this amount in

interest:

+

$

0

You were charged this amount in fees: +

$

0

You paid or were credited this

amount toward the debt:

–

$

33,000.0

0

Total amount of the debt now:

$

25 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

Step 4: Determine the current

debt amount.

Enter the current account balance

as of the date the validation

information is provided (September

15, 2022).

This is the completed Itemization

Table ABC Financial, Inc., included

in the validation notice.

As of August 15, 2021, you owed:

$

40,000.00

Between August 15, 2021 and today:

You were charged this amount in

interest:

+

$

0

You were charged this amount in fees: +

$

0

You paid or were credited this

amount toward the debt:

–

$

33,000.0

0

Total amount of the debt now:

$

7,000

.00

Multiple Debts

A debt collector who is collecting multiple debts owed or alleged to be owed by the same consumer

may provide 1) a separate validation notice for each debt, or 2) depending on the facts and

circumstances, a single validation notice that combines some or all of the debts.

As stated above, this guidance document assumes use of the model validation notice, and, as such,

use of the Itemization Table, to obtain a safe harbor for the Rule’s validation information content

and format requirements. A debt collector could receive that safe harbor when disclosing multiple

debts on a single validation notice where 1) the debts are owed or alleged to be owed by the same

consumer, 2) the debts are owed to the same creditor, and 3) the debts have a common itemization

date.

A debt collector disclosing multiple debts would not obtain the validation information content and

format requirements safe harbor for use of the model validation notice if it included multiple

Itemization Tables on the model validation notice itself.

However, a debt collector disclosing multiple debts on a single model validation notice to obtain

that safe harbor may do one of the following:

1. Include a cumulative itemization of the Itemized Amounts in the Itemization Table on the

model validation notice, reflecting the required information for all of the relevant debts in one

table; or

26 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

2. Include an Itemization Table on the model validation notice with a statement referencing

separate page(s) where the Itemized Amounts are disclosed. The debt collector would include

a separate itemization of each debt on one or more pages in the same communication with the

model validation notice. Comment 1006.34(c)(2)(viii)-4.

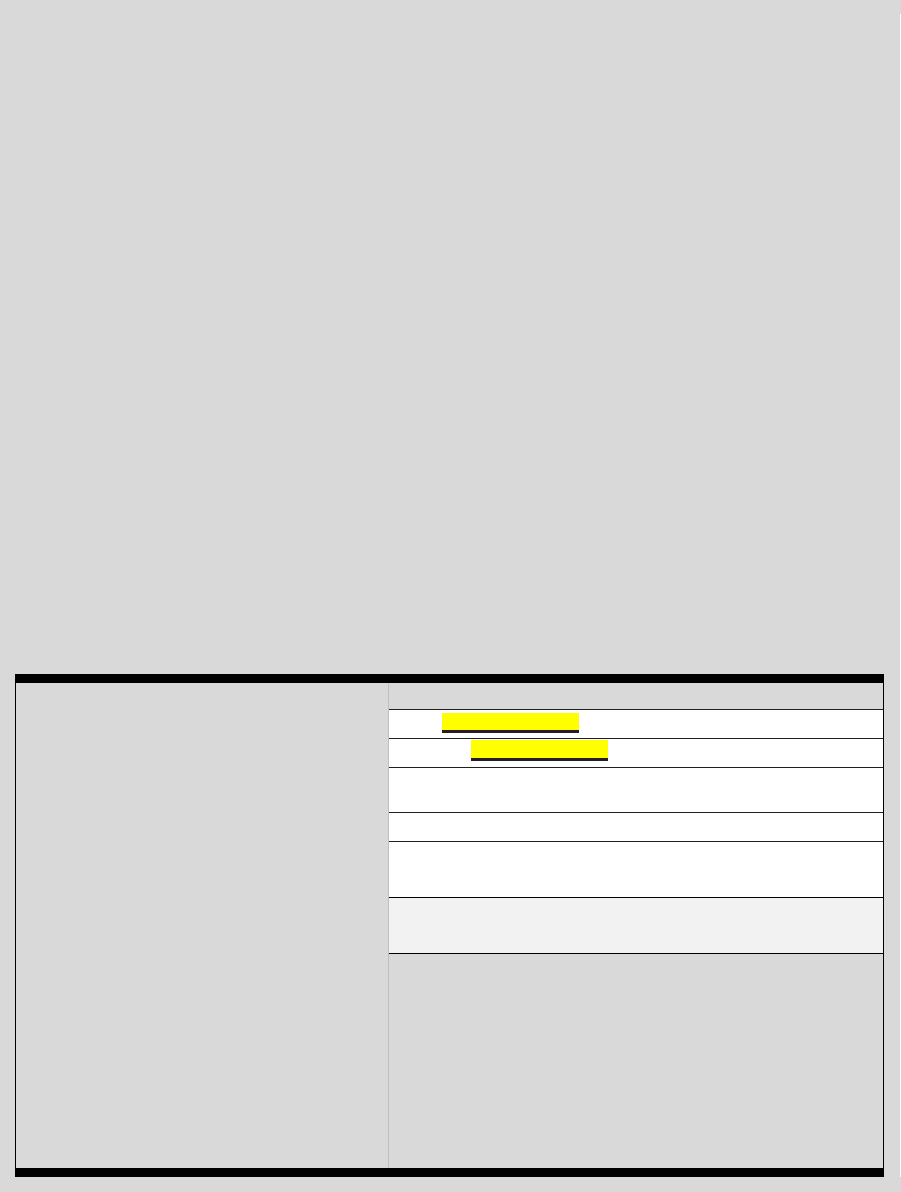

An illustration of how a debt collector may complete the Itemization Table on the model validation

notice for each of these options is shown in Figure 6.

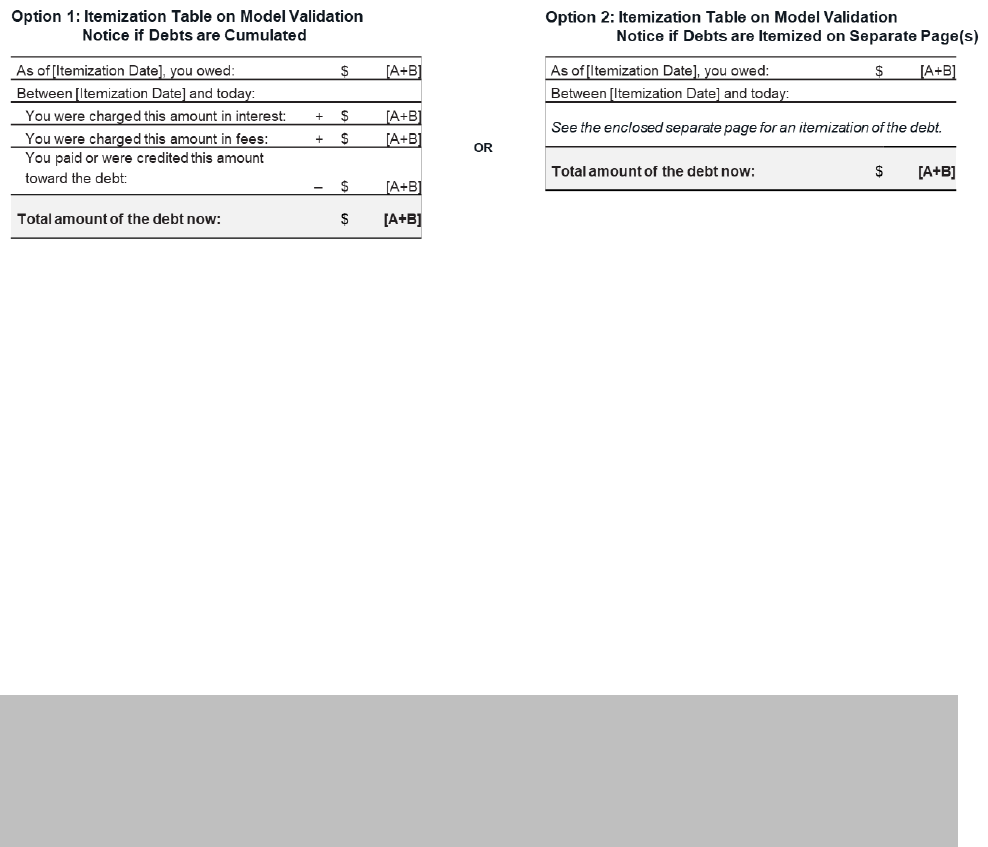

FIGURE 6: EXAMPLE OF COMPLIANT ITEMIZATION TABLES FOR MULTIPLE DEBTS

A debt collector who chooses to obtain the safe harbor for validation information content and

format requirements by using the model validation notice would be compliant if it disclosed

multiple debts in a single, cumulative format on the model validation notice following the steps in

this guidance document to produce an Itemization Table like the table shown in Option 1 in the

figure above.

In doing so, the debt collector would, in Step 1, select and provide one itemization date, a date that

is the same for each debt. For Step 2, for multiple debts disclosed this way, the amount of the debt

as of the itemization date is the sum of the amount of the debts as of that date. For Step 3, the

debt collector would provide the Itemized Amounts in a single, cumulative itemization, with a

cumulative sum for each field. For Step 4, the current amount of the debt is a single, cumulative

figure that would be the sum of all the debts. Comment 1006.34(c)(2)(ix)-2.

Example: Single Validation Notice with Cumulative Itemization Table

Assume that a debt collector is collecting a consumer’s three medical debts that include a

hospital stay debt, radiology services debt, and physical therapy services debt. These debts are

all from the same creditor. The debt collector chooses to combine the three debts in a single

27 DEBT COLLECTION RULE: DISCLOSING THE VALIDATION INFORMATION VERSION 1.0 (10/2021)

ITEMIZATION TABLE

validation notice and chooses to provide a cumulative Itemization Table. Using the process

discussed above, the debt collector would do the following:

Step 1: Select one itemization date that applies for all the debts.

Step 2: Using that date, determine the amount of each of the debts as of that itemization date

and disclose the cumulative sum of those amounts.

Step 3: Calculate any Itemized Amounts that have accrued during the Itemization Period for all

three debts and disclose each of the applicable fields of the Itemization Table with the relevant

cumulative sums.

Step 4: Finally, sum the current amount of debt for all three debts.

A debt collector who chooses to obtain the safe harbor for validation information content and

format requirements by using the model validation notice would also be compliant if it disclosed

multiple debts by providing separate itemizations for each debt on a separate page(s) in the same

communication as the validation notice. The debt collector would still be required to disclose the

Itemization Table on the validation notice, and could disclose the table as shown in Option 2 in

Figure 6.

As shown in that table, the debt collector would be compliant if it disclosed a single itemization

date for Step 1, one cumulative amount of the debt as of that date for Step 2, and a cumulative

current debt amount for Step 4. However, for Step 3, the debt collector must include in the

Itemization Table a reference to the separate page(s) and then provide the separate itemizations

on a separate page or pages. Comment 1006.34(c)(2)(viii)-4.

12

Nothing in the Rule prohibits a

debt collector from repeating the information in Steps 1, 2, or 4 on the separate page(s) with the

Itemized Amounts from Step 3.

12

As noted in footnote 8, a debt collector may provide the itemization of the current amount of the debt on a separate

page(s). Comment 1006.34(c)(2)(viii)-4; Comment 1006.34(c)(2)(viii)-3. However, the debt collector does not

receive a safe harbor for the content and format requirements for any information included on the separate page(s).

12 CFR 1006.34(d)(2)(ii).