9/27/2016

1

©

Bradley Arant Boult Cummings LLP ***THIS IS NOT INTENDED TO PROVIDE LEGAL ADVICE***

Financial Services Webinar Series

CFPB Mortgage Servicing

Amendments

Part 3. What You Need to Know: Bankruptcy

September 27, 2016

Presented by:

Jonathan Kolodziej, Chris Hawkins, and Alexandra Dugan

Timeline

2

November

20, 2014

• CFPB issues proposed rule and opens comment period

March 16,

2015

• Comment period on proposal closes

• To date, CFPB has received and posted 200 comments

April 26,

2016

• Report summarizing testing of bankruptcy periodic statement

forms is published in the Federal Register and reopens comment

period

May 26,

2016

• Comment period on report and testing method/results closes

• To date, CFPB has received and posted 20 comments

August 4,

2016

• CFPB releases final amendments to existing rules in Regulations

X and Z, along with interpretive rule on FDCPA compliance

9/27/2016

2

Summary

Initial release of Mortgage Servicing Rules did not contain exemptions

for borrowers in bankruptcy, but Interim Final Rule issued October 2013

granted a reprieve with respect to problematic communication

requirements

The 2016 Final Rule contains bankruptcy requirements covering

primarily two key topics:

1. Early Intervention

2. Periodic billing statements

In the absence of a bankruptcy exemption or bankruptcy-specific

modification, the Mortgage Servicing Rules apply to loans in bankruptcy

Effective date:

• 18 months from date published in Federal Register for periodic billing

statement requirements for borrowers in bankruptcy

• 12 months from date published in Federal Register for early intervention

requirements

3

Early Intervention

4

9/27/2016

3

Early Intervention – Live Contact

Current Rule

• A servicer shall contact the borrower no later than the 36

th

day of delinquency, and promptly inform the borrower of

loss mitigation options, if appropriate

• This is a recurring obligation for each delinquency

• Servicers are exempt from the early intervention

requirements while the borrower is a debtor in bankruptcy

Amended Rule

• Exemption for live contact remains intact while any

borrower on an account is a debtor in bankruptcy

• Adds clarity regarding when a servicer must resume

compliance

5

Early Intervention – Written Notice

Current Rule

• A servicer must provide the borrower with an early

intervention written notice not later than the 45th day of the

borrower's delinquency

This is a recurring obligation, but the written notice does not

have to be sent more than once during any 180-day period

• Servicers are exempt from this requirement while the

borrower is a debtor in bankruptcy.

Amended Rule

• Partial exemption for the written notice obligation

• Modified timing requirements

• Modified content for written notice

• Provides clarity regarding when a servicer must resume full

compliance

6

9/27/2016

4

Early Intervention – Written Notice

Partial Exemption

• While any borrower on a mortgage loan is a debtor in

bankruptcy, the servicer, with respect to that mortgage loan,

is exempt from the written notice requirement if

No loss mitigation option is available, or

Any borrower on the mortgage loan has provided a cease

communication request in accordance with Section 805(c) of

the FDCPA

7

Early Intervention – Written Notice

Modified Timing

• If a borrower is delinquent when the bankruptcy petition

under title 11 of the United States Code is filed, written

notice must be sent no later than 45 days after the filing

• If the borrower is not delinquent when the bankruptcy

petition is filed, but subsequently becomes delinquent while

a debtor in bankruptcy, written notice must be provided not

later than the 45th day of the borrower’s delinquency

• Modified timing requirements apply regardless of whether

the servicer provided the written notice in the preceding

180-day period

• Early Intervention written notice is not required more than

once during a single bankruptcy case

8

9/27/2016

5

Early Intervention – Written Notice

Modified Content

• Content requirements of §1024.39(b)(2) still apply:

Statement encouraging borrower to contact servicer;

Telephone number for assigned servicer personnel;

If applicable, a brief description of examples of loss mitigation

options that may be available;

If applicable, either application instructions or statement

regarding how the borrower can obtain more information; and

HUD counseling information

• Early Intervention written notice may not contain a request

for payment when sent to a borrower that is a debtor in

bankruptcy

9

Early Intervention

Resuming Compliance

• A servicer that was exempt due to a borrower’s bankruptcy

must resume compliance after the next payment due date

that follows the earliest of the following events:

The bankruptcy case is dismissed;

The bankruptcy case is closed; and

The borrower reaffirms personal liability for the mortgage loan

• Live contact and written notice exemptions continue to

apply with respect to a mortgage loan for which the

borrower has discharged personal liability

Must resume compliance with the modified written notice

requirements if the borrower has made any partial or periodic

payment after commencement of the bankruptcy case

10

9/27/2016

6

Early Intervention

CFPB Rationale for Written Notice Requirements

• The CFPB sought to balance the desire to provide

information about loss mitigation options to borrowers

in bankruptcy with the concerns about sending

communications that could be viewed as stay

violations

Key Considerations/Takeaways

• Servicers should ensure that bankruptcy milestones

are accurately and quickly updated in the system of

record

• The early intervention amendments become effective

12 months after the publication date

11

Periodic Billing Statements

12

9/27/2016

7

Periodic Billing Statements

Borrowers in Bankruptcy

Current Rule

• Periodic billing statements must be provided for each billing

cycle, unless an exemption applies

• A servicer is exempt from sending periodic billing

statements for a mortgage loan while the consumer is a

debtor in bankruptcy

Amended Rule

• Servicers must send modified periodic billing statements to

borrowers in bankruptcy, unless the borrower is exempt

• Modified content requirements

• When a modified statement is required, the modified

statement may be sent to any or all primary obligors, even if

one of the primary obligors is not a debtor in bankruptcy

13

• Billing statements are not required if:

The borrower is in a bankruptcy case or the borrower has

discharged personal liability for the mortgage loan pursuant to

11 U.S.C. 727, 1141, 1228, or 1328; and

o The borrower requests that the servicer cease providing

a periodic statement or coupon book in writing;

o The plan provides for a surrender, avoidance of the lien

or does not provide for, the payment of pre-bankruptcy

arrearage or the maintenance of payments due;

o The bankruptcy court order provides for the lien to be

avoided, the stay to be lifted or for the servicer to cease

providing a periodic statement or coupon book in writing;

or

o A statement of intention is provided for surrender and the

borrower has not made a partial or complete payment

after the bankruptcy case

14

Periodic Billing Statements

Bankruptcy Exemption

9/27/2016

8

• Exemption no longer applies if:

The debtor reaffirms personal liability; or

Any consumer on the loan requests in writing that the servicer provide

periodic statements

o Unless a court enters an order requiring the servicer to cease

sending statements

• A servicer may establish an address that the consumer must use

to request to opt in or opt out of periodic statements

Same address must be designated for opt-in and opt-out requests

Servicer must notify the consumer of the address in a manner that is

reasonably designed to inform the consumer of the address

A consumer’s written request to opt-in or opt-out is effective as of the

date of receipt by the servicer

15

Periodic Billing Statements

Bankruptcy Exemption

Periodic Billing Statements

Bankruptcy Exemption

• Servicer must transition to sending a modified billing

statement, or back to an unmodified billing statement, when

any of the following triggers applies:

Borrower becomes a debtor in bankruptcy

Borrower ceases to be a debtor in bankruptcy

Servicer ceases to qualify for an exemption from the billing

statement requirements

• Transitional single-billing-cycle exemption

Servicers are exempt from sending a billing statement for a

single billing cycle when one of the above trigger events

occurs within 14 days of the next payment due date

• Timing of first modified or unmodified statement after

transition

Mailed within a reasonably prompt time after first payment due

date or end of courtesy period

16

9/27/2016

9

Periodic Billing Statements

Bankruptcy Exemption

CFPB Rationale for Exemption Requirements

• The exemptions are tailored to apply to borrowers who have

provided some indication that they do not intend to retain

the property or affirmatively requested not to receive

periodic statements

Key Considerations/Takeaways

• Servicers should ensure that their system of record

accurately tracks data points to determine whether an

exemption applies, such as surrender or lift of stay.

• Servicers should ensure that reliable logic is utilized to

identify when a borrower in bankruptcy is exempt from the

periodic statement requirement.

17

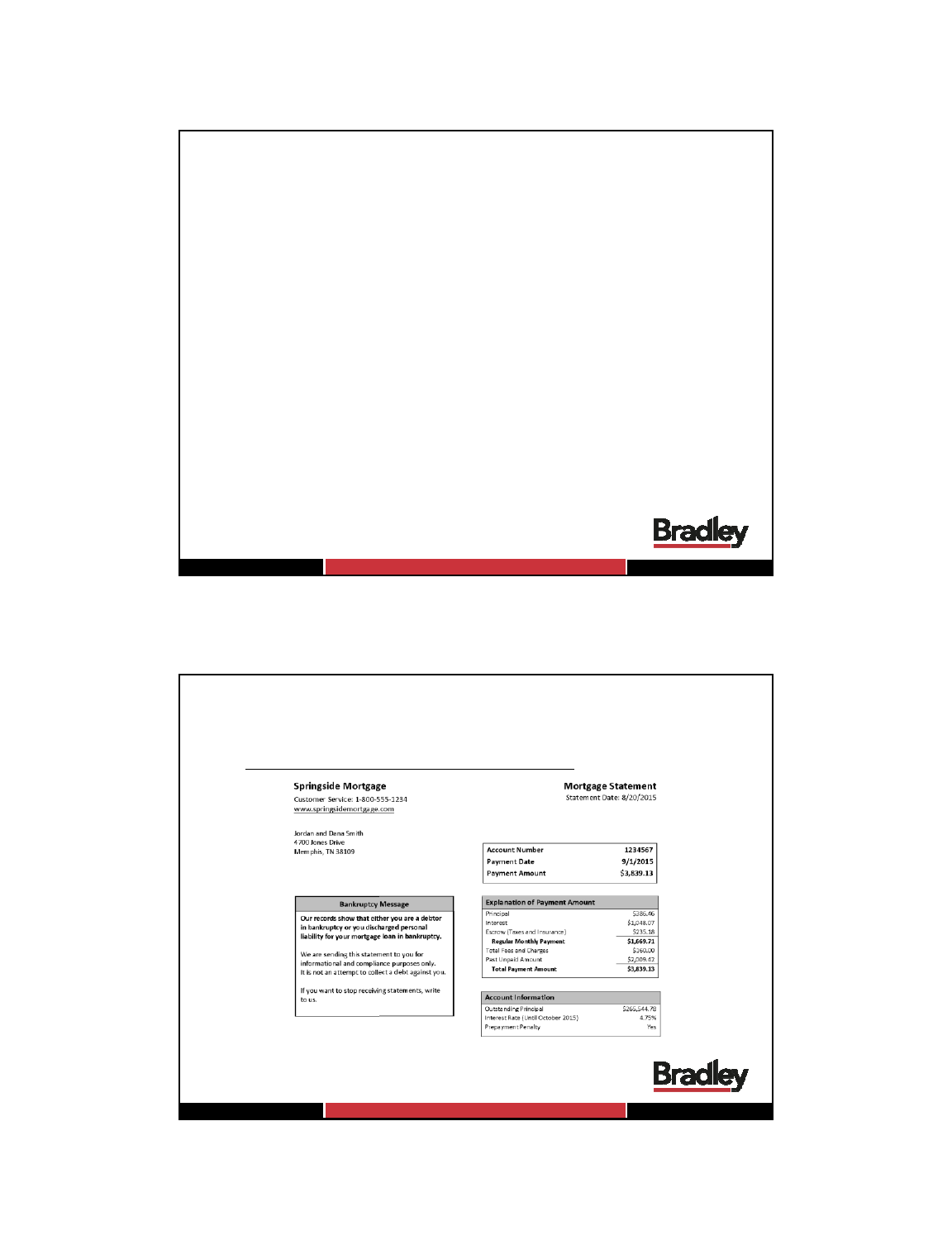

Periodic Billing Statements

Content

• Servicers must provide a periodic statement or coupon

book to consumers in bankruptcy (or that have received a

discharge in bankruptcy), with modifications to account for

the bankruptcy status and the specific chapter of bankruptcy

in which the consumer is a debtor

• Sample forms

CFPB provided a sample form for accounts in Chapter 7 or 11,

and a separate sample form for accounts in Chapter 12 or 13

• Servicers may use terminology other than that found on the

samples, so long as the new terminology is commonly

understood

• Statements may be modified as necessary to facilitate

compliance with applicable law or a court order

18

9/27/2016

10

Periodic Billing Statements

Content

• CFPB rationale for modified content requirements:

The benefit to consumers of providing the modified

information in the periodic statements outweighs the

burden on servicers

The disclosures and modifications to the account

information will mitigate the risk that a statement violates

the automatic stay and/or discharge order

The information required on the modified Chapter 12/13

periodic statements will assist consumers in making

timely payments and tracking progress in their cases

Even with respect to Chapter 7 cases in which the

consumer has received a discharge, periodic statements

can assist the consumer in making the payments

necessary to retain the residence.

19

Periodic Billing Statements

Content

Key Considerations/Takeaways

• Modified statements remove essentially all references to

delinquency/late payments

• The servicer may use “contractual” basis for applying all

payments received instead of a “bankruptcy” basis.

• The servicer still must be able to provide a running

accounting with respect to the consumer’s progress toward

repaying the prepetition arrearage

• There still may be a gap with respect to when post-petition

“ongoing” payments from a trustee should be considered

delinquent.

20

9/27/2016

11

Periodic Billing Statements

Content – All Bankruptcy Types

• Statement (or coupon book) may omit:

The amount of any late payment fee, and the date on

which that fee will be imposed if payment has not been

received

The length of the consumer’s delinquency

The possible risks, such as foreclosure, and expenses,

that may be incurred if the delinquency is not cured

A notice of whether the servicer has made the first

notice or filing required by applicable law for any judicial

or non-judicial foreclosure process, if applicable

21

Periodic Billing Statements

Content – All Bankruptcy Types

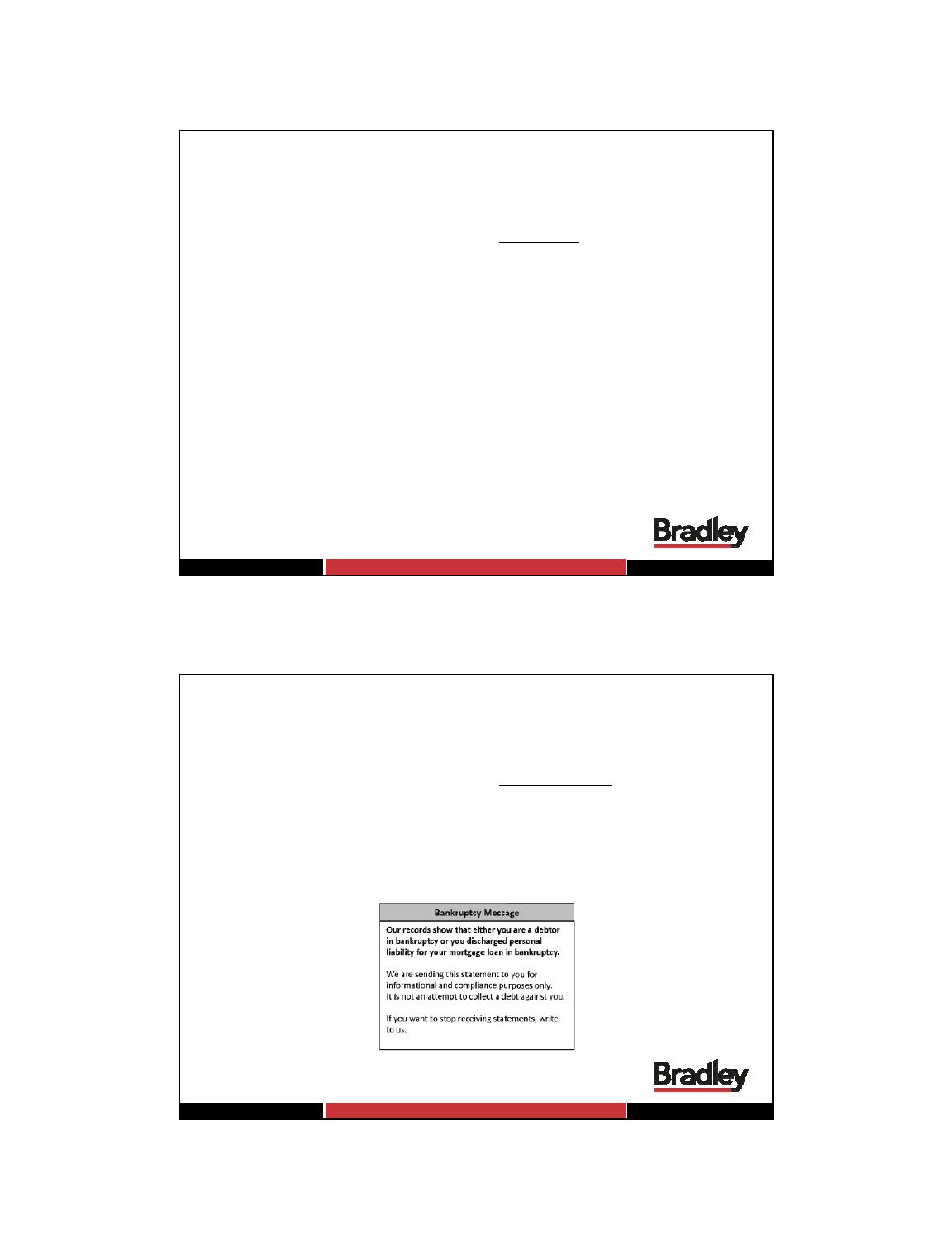

• Statement (or coupon book) must include:

A statement identifying the consumer’s status as a

debtor in bankruptcy or the discharged status of the

mortgage loan

A statement that the periodic statement is for

informational purposes only

22

9/27/2016

12

Periodic Billing Statements

Content – Chapters 12 and 13

• With respect to a mortgage loan in which any consumer with

primary liability is a debtor in a Chapter 12 or Chapter 13

case, additional modifications apply

• Statements (or coupon books) may omit certain information

that is normally required when the consumer is more than 45

days delinquent:

Account history showing the previous six months or the period

since the last time the account was current, whichever is shorter

A notice indicating any loss mitigation program to which the

consumer has agreed, if applicable

The total payment amount needed to bring the account current

HUD counseling information

23

Periodic Billing Statements

Content – Chapters 12 and 13

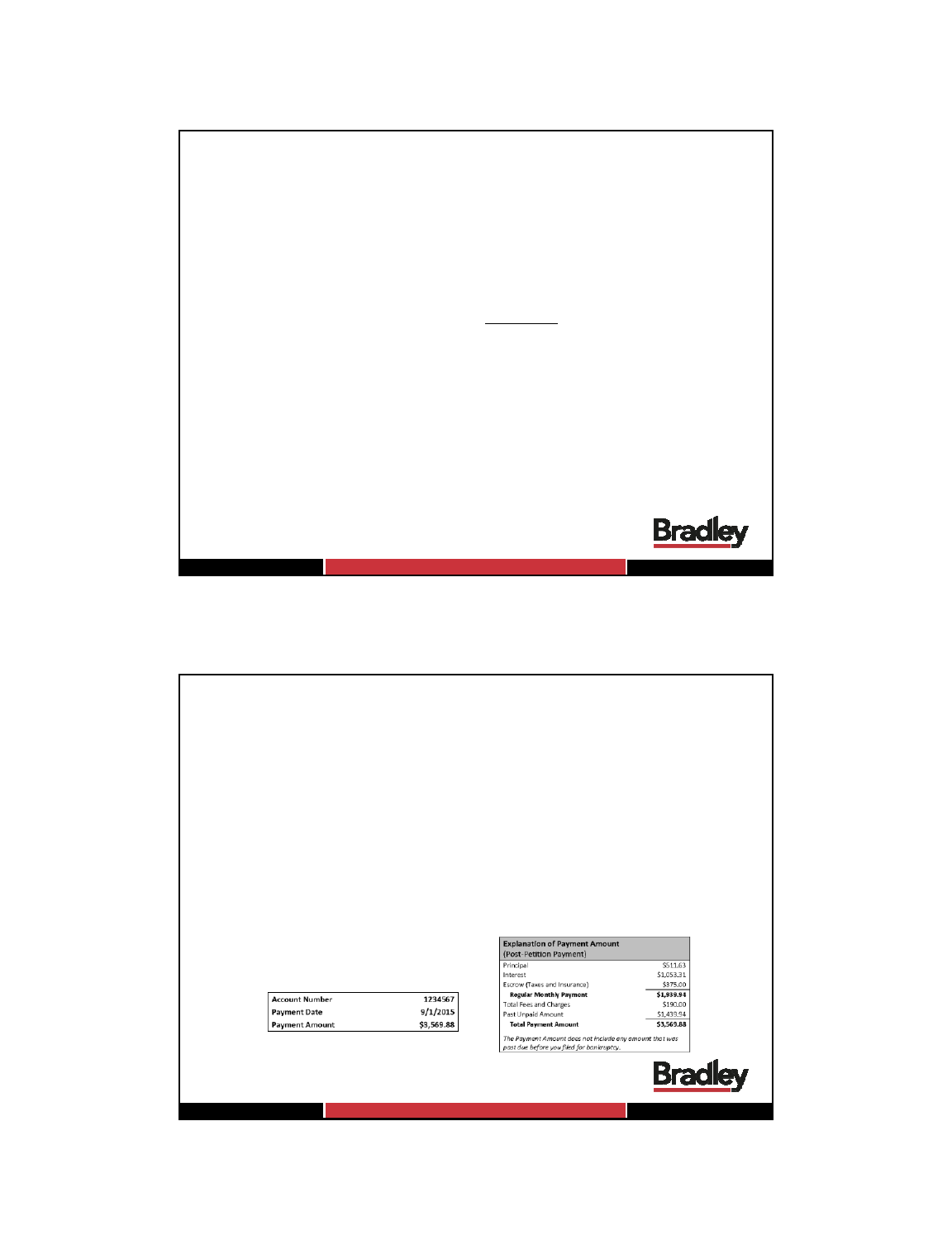

• Amount Due on statement (or coupon book) may be limited to:

Date and amount of post-petition payment due; and

Any post-petition fees and charges imposed by the servicer

• Explanation of Amount Due on statement (or coupon book)

may be limited to:

Monthly post-petition payment amount, including a breakdown

showing how much, if any, will be applied to principal, interest

and escrow;

Total sum of any post-petition fees or charges imposed since the

last statement; and

Any post-petition payment

amount past due

24

9/27/2016

13

Periodic Billing Statements

Content – Chapters 12 and 13

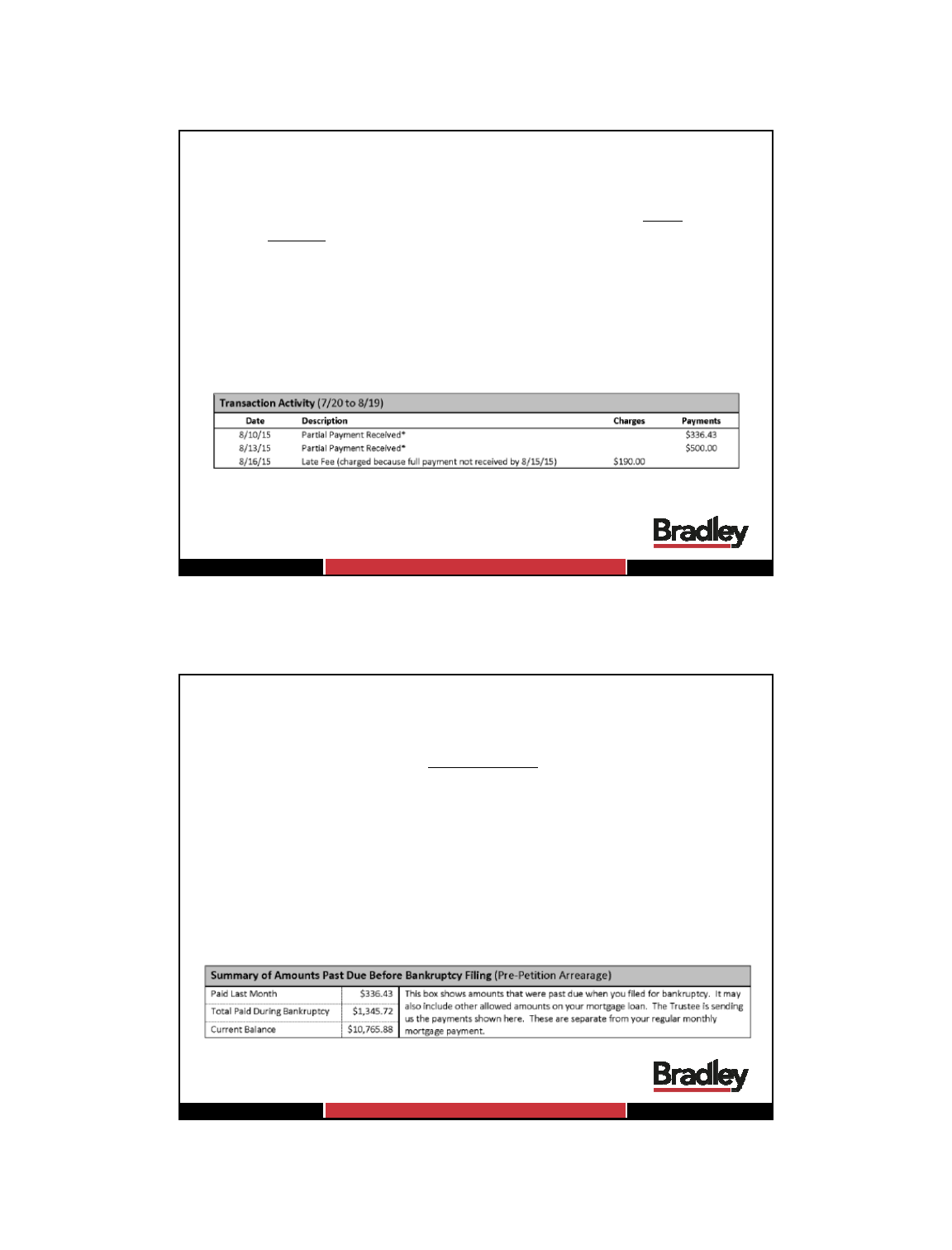

• Transaction Activity on statement (or coupon book) must

include:

All post-petition payments

All pre-petition payments

Payments of post-petition fees and charges

Post-petition fees and charges the servicer has imposed since

last statement

• Source of payments need not be identified

25

• If applicable, servicer must disclose information regarding

the pre-petition arrearage:

Total of all pre-petition payments received since last statement

Total of all pre-petition payments received since beginning of

the consumer’s bankruptcy case

Current balance of the consumer’s pre-petition arrearage

• These items must be grouped in close proximity to each

other and located on the first page of the statement, or,

alternatively, on a separate page enclosed with the periodic

statement or in a separate letter

26

Periodic Billing Statements

Content – Chapters 12 and 13

9/27/2016

14

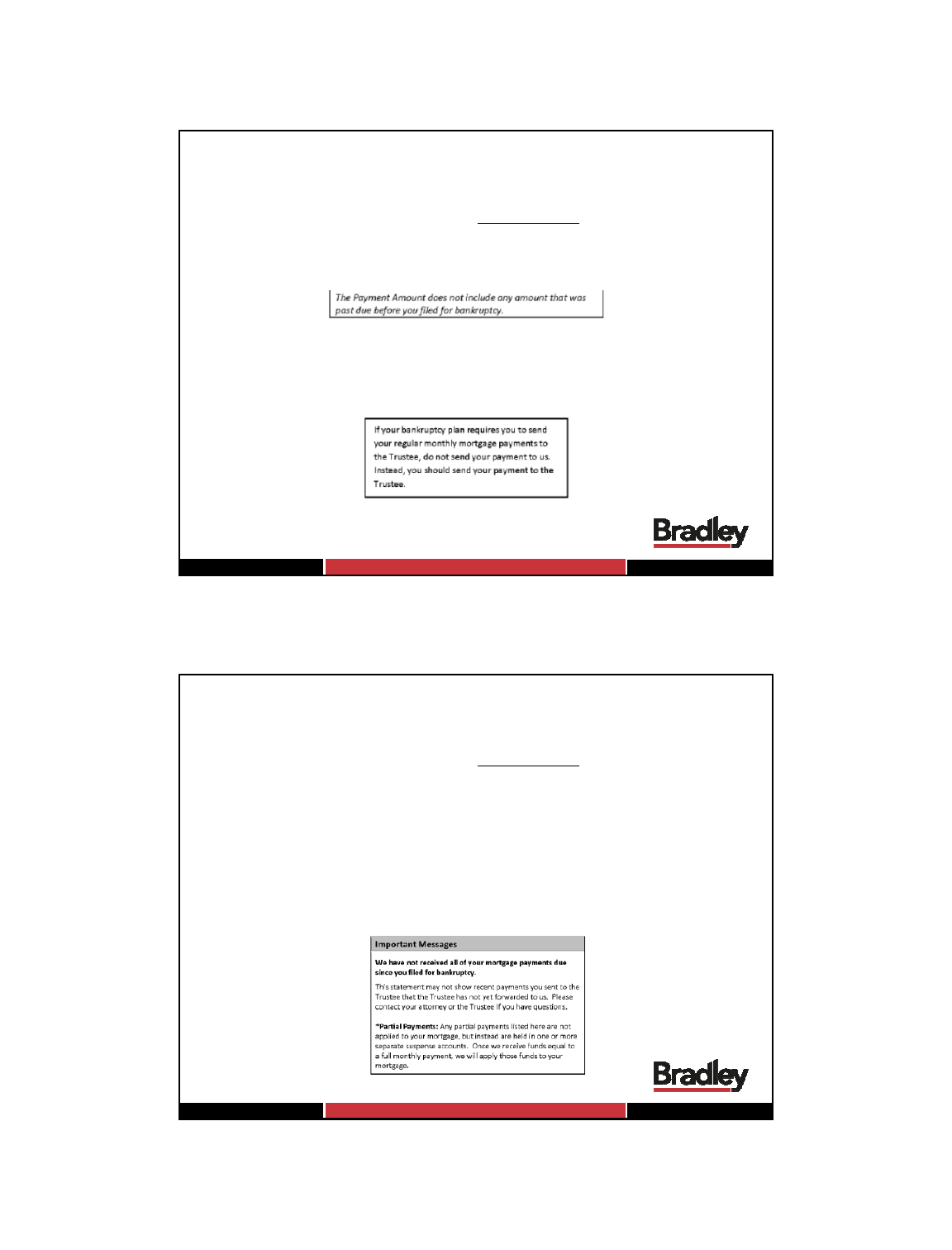

• Statement (or coupon book) must include, as applicable:

A statement that the amount due includes only post-petition

payments and does not include other payments that may be

due under the terms of the consumer’s bankruptcy plan

If the consumer’s bankruptcy plan requires the consumer to

make the post-petition mortgage payments directly to a

bankruptcy trustee, a statement that that the consumer should

send the payment directly to the trustee and not the servicer

27

Periodic Billing Statements

Content – Chapters 12 and 13

• Statement (or coupon book) must include, as applicable:

A statement that the information disclosed on the periodic

statement may not include payments made to the trustee and

may not be consistent with the trustee’s records

A statement that encourages the consumer to contact his/her

attorney or the trustee regarding the application of payments

If the consumer is more than 45 days delinquent on post-

petition payments, a statement that the servicer has not

received all the payments that became due since the

consumer filed for bankruptcy

28

Periodic Billing Statements

Content – Chapters 12 and 13

9/27/2016

15

Periodic Billing Statements

Coupon Books

• Required disclosures may be included anywhere in the

coupon book provided to the consumer, or on a separate

page enclosed with the coupon book

• Upon request, servicer must make available to the consumer

(by telephone, in writing, in person, or electronically if

consumer consents) the pre-petition arrearage information

• The same “general” bankruptcy modifications apply to

coupon books

• Delinquency/foreclosure information may be omitted

• Other accounting information

o Amount Due

o Explanation of Amount Due

o Transaction Activity

o Additional Disclosures

29

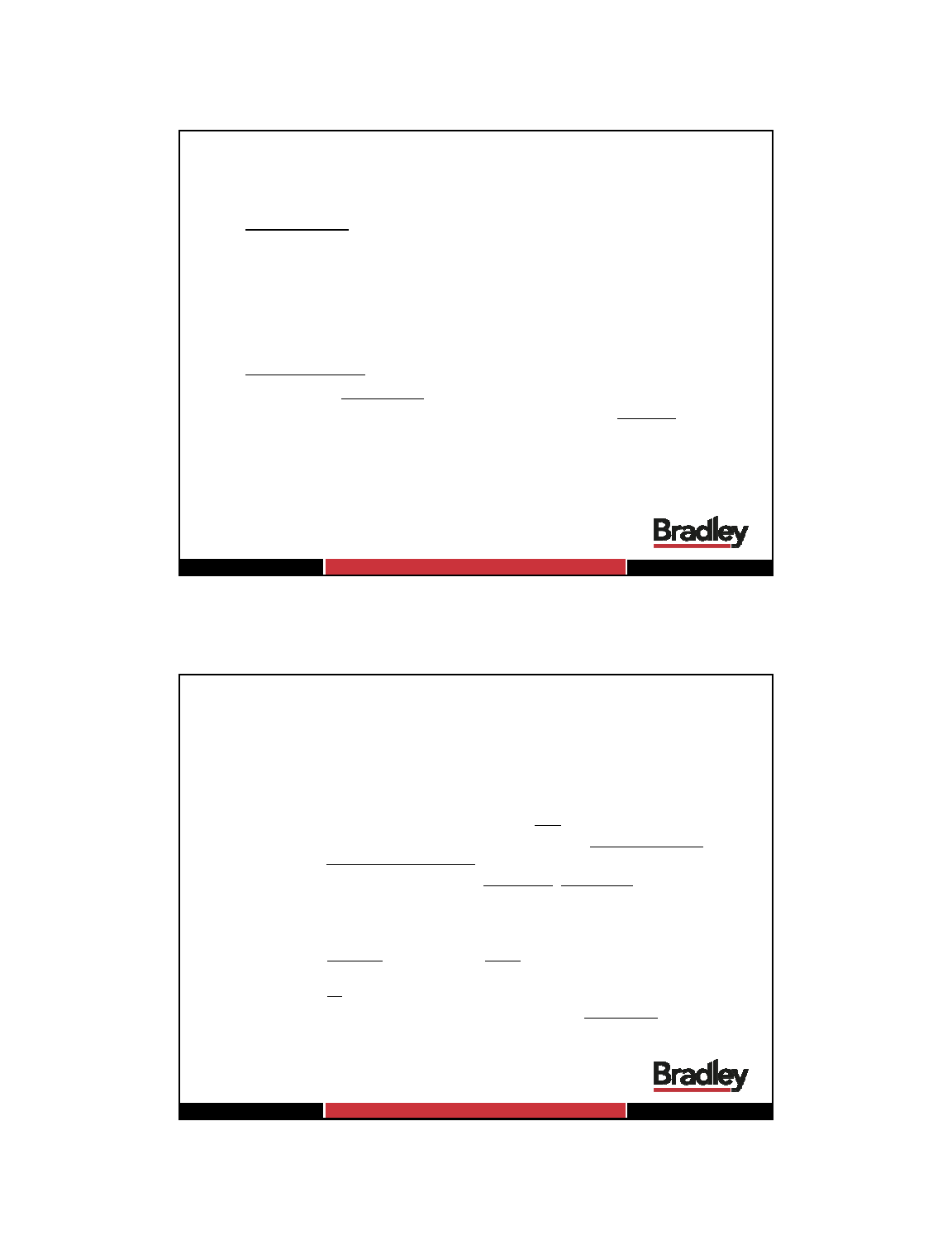

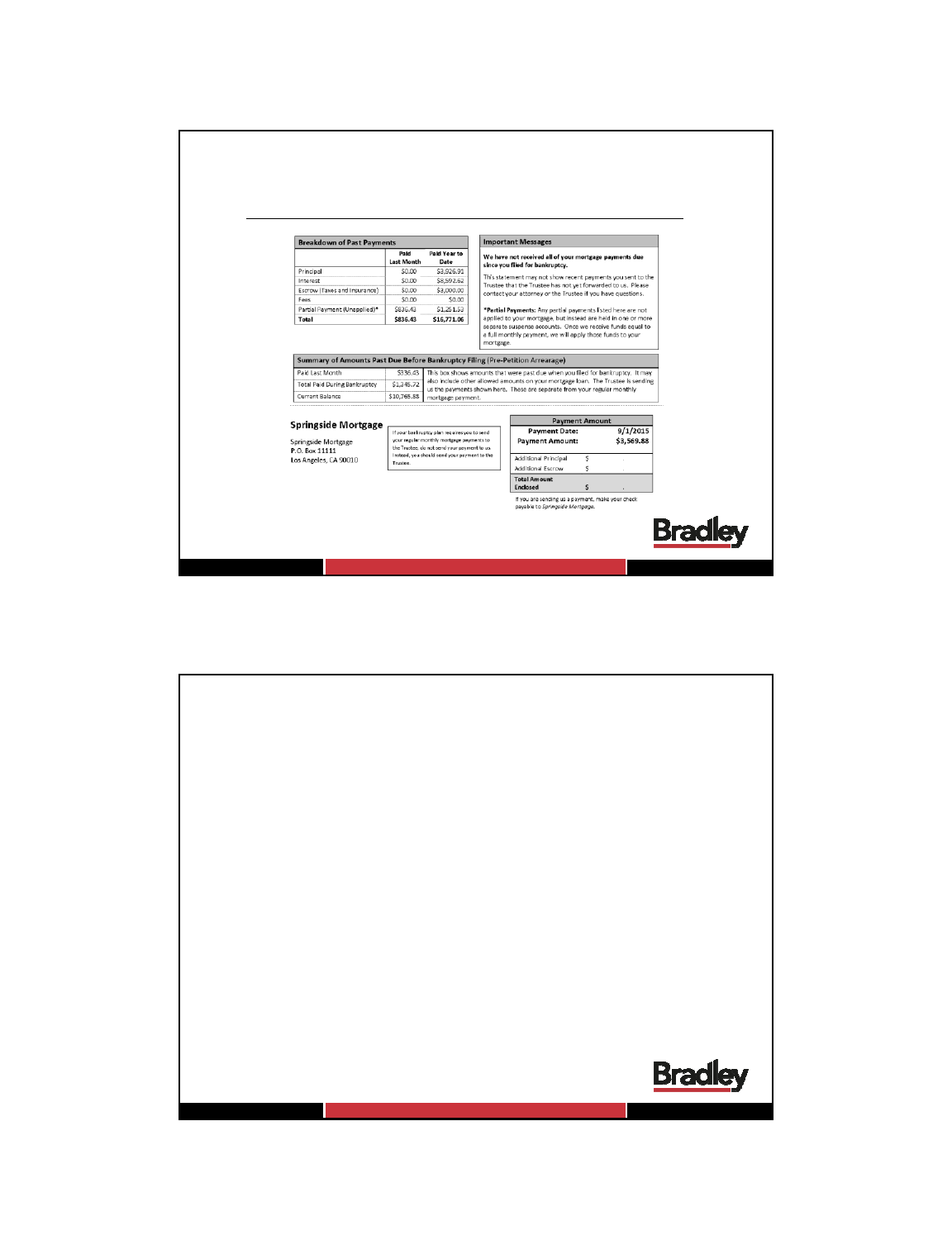

Periodic Billing Statements

Sample Forms

Chapter 7/11 Sample Periodic Statement

30

9/27/2016

16

Chapter 7/11 Sample Periodic Statement (continued)

31

Periodic Billing Statements

Sample Forms

Chapter 12/13 Sample Periodic Statement

32

Periodic Billing Statements

Sample Forms

9/27/2016

17

Chapter 12/13 Sample Periodic Statement (continued)

33

Periodic Billing Statements

Sample Forms

Key Considerations &

Takeaways

34

9/27/2016

18

Borrowers in Bankruptcy

Key Considerations & Takeaways

• Successfully implementing the requirements specific to

borrowers in bankruptcy will be a challenge

CFPB recognized that, with respect to billing statement

requirements:

o “[S]ervicers and third-party service providers need sufficient

time to coordinate, develop, and test systems required to

modify periodic statements for consumers in bankruptcy”

o Servicers “also need sufficient time to train employees

regarding the bankruptcy periodic statement requirements”

• Servicers should begin implementation efforts as soon as

possible

Map out applicable requirements

Conduct gap analyses

Evaluate system and technological needs

Coordinate with impacted areas of business

Monitor for additional CFPB guidance

35

Questions?

Alexandra Dugan

adugan@bradley.com

615.252.4638

Chris Hawkins

chawkins@bradley.com

205.521.8556

Jonathan Kolodziej

jkolodziej@bradley.com

205.521.8235

9/27/2016

19

Thank You

See below for upcoming webinars in this series.

Date Webinar

October 6, 2016

11:30 AM - 12:30 PM CST

What You Need to Know: Loss Mitigation

Jonathan Kolodziej, Jason Bushby